Rockefeller Institute Visiting Scholar Jim DeWan recently wrote that the Trump administration would have to show its cards on the Affordable Care Act (ACA). Specifically, DeWan suggested that how the administration addressed Cost Sharing Reduction subsidies — the provision in the ACA where insurance companies participating in exchanges receive federal subsidies in order to reduce enrollees’ out-of-pocket costs and keep individual health premiums down by stabilizing the market — would show how it would handle the ACA more generally. Some background: the subsidy is playing out through a court case brought by the House Republicans. The House challenged the subsidies and won the lower court case, but the court has allowed for the subsidies to continue as the case winds its way through the judicial process.

The administration had options: it could actively try and dismantle the ACA by eliminating the subsidy program administratively or by withdrawing the government’s appeal of the lower court ruling, or the administration could let the ACA run its course while trying to repeal and replace the law through Congress.

As of now, the Trump administration has straddled both options by filing an extension in the case for only three months, but not actively dismantling the program. According to media reports, the president has also indicated his desire to end these payments. This short-term extension has nonetheless created uncertainty in the markets, and insurers have taken it as a strong signal that the Trump administration will more than likely eliminate the subsidies. This signal is having the effect the administration presumably wanted: showing that the ACA isn’t working.

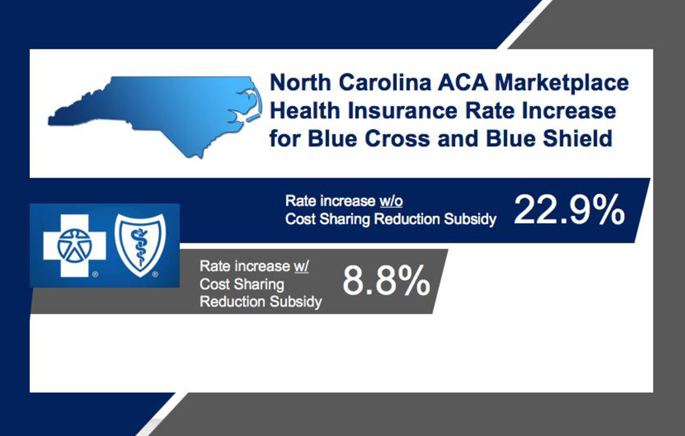

In North Carolina (one of the 40 states the Rockefeller Institute and its partners have been studying as part of the ACA Implementation Network), the state’s dominant health provider, Blue Cross and Blue Shield, recently announced it would raise health-insurance rates for individual policies under the Affordable Care Act nearly 23 percent because of the Trump administration’s signaling it will eliminate the federal cost sharing reductions that help keep premiums down. If the federal government kept the subsidy in place, Blue Cross and Blue Shield claimed it only would have increased rates by 8.8 percent.

The elimination of the Cost Sharing Reduction subsidies, and subsequent increase in premiums, will have greater effects in states where lawmakers have opposed the ACA. In North Carolina, for example, the double-digit rate increase comes on top of state-specific burdens that make implementation more expensive and difficult. As Wake Forest University’s Mark Hall examined in his report, A Study of the Affordable Care Act Competitiveness In North Carolina, because North Carolina (like some other states) refused to concurrently expand its Medicaid program, Medicaid-eligible individuals were forced to join the health insurance marketplace, resulting in increased prices. In order to stave off financial loses in the Marketplace, Blue Cross and Blue Shield has already increased prices 32 percent in 2016 and 24 percent in 2017. Blue Cross and Blue Shield’s proposed double-digit increase is on top of the previous hikes.

Even before this proposed increase, North Carolina already has some of the highest health premiums in the nation in the ACA marketplace. Our joint report, citing the Kaiser Family Foundation, found North Carolina had the fourth highest premiums in the country in 2016 under lower-cost health insurance plan options, and the second highest average premiums in the nation in 2016.

A greater year-over-year increase in health insurance premiums has real impacts on families and individuals. In North Carolina, more than 600,000 people are enrolled in the marketplace, which is the fourth highest number in the nation. Double-digit increases may simply make the plans cost prohibitive to many. Blue Cross and Blue Shield is virtually the only game in town in North Carolina, so it’s not as if individuals can shop for a better priced plan.

Whether this event is the straw that breaks the proverbial camel’s back and sinks the ACA in North Carolina remains to be seen. Clearly, the proposed elimination of the Cost Sharing Reduction subsidies is having an effect, and families will have to pay more for their healthcare. Whether it is too much remains to be seen, but families are the unfortunate guinea pigs in this experiment.

[1] Special thanks to Patricia Strach, Jim DeWan, and Thomas Gais for their help on the piece.