January 6, 2011

The “Great Recession” of 2007 to 2009 has taken a great toll on housing markets in most cities and metropolitan areas in all parts of the country. Though the pace and extent of the overall economic recovery of these markets is still far from certain, many places will likely resume growth and fully recover within the next decade or so. This is almost certainly not to be the case for all metropolitan areas. In fact, a number of large metropolitan statistical areas (MSAs) experienced severe recessions during the latter half of the 20th century and prior to the Great Recession and never fully recovered or took many years to do so. Even among those metro areas with relatively bright long-run prospects for growth, certain submarkets within them may remain well below recent house price peaks for many years to come.

What is a declining city? Simply put, a declining city is one in which the people have left, but the houses, apartment buildings, offices and storefronts remain. At the extreme, think of a ghost town from the Old West, a town that lost its reason for being. Are there cities or large metro areas in the United States at risk of disappearing back into the desert (or the swamp) today? Probably not, but there are certainly neighborhoods and submarkets within metro areas that have passed a tipping point, and have little prospect of returning to anything close to their previous peaks. Lastly, another type of declining city may also be emerging — places that grew substantially during the housing boom and are now experiencing unprecedented declines in house prices and increases in foreclosures.

The primary goal of this paper is to offer insights on the potential future evolution of real estate markets in cities that are in the midst of a severe and persistent economic decline. Through a review of a massive and interdisciplinary body of prior research, analysis of new empirical evidence on the experiences of many large U.S. metro areas over the past 40 years and a focus on the experiences of seven large metro areas since 2000, including during the Great Recession, I seek answers to three questions:

The answers to these questions are based upon review of the literature and new empirical analysis. Several different sources of data are utilized in order to highlight some of the challenges and opportunities for future or additional empirical work in this field of inquiry. Of particular interest for the last two questions is the incidence of extreme outcomes that threaten the long-term viability of neighborhoods or submarkets within declining cities.

My conclusions are as follows:

Though I tend to think a decline in housing demand will be persistent in many metropolitan markets, this is a tough call and the best opinions will recognize the importance of specific local market conditions. The analyses in this paper suggest there will be and already have been substantial threats to the viability of certain neighborhoods. This, I think, is a critical point that will likely be well understood by potential home buyers and lenders, who want to avoid places plagued by high foreclosures, vacancies and a deteriorating housing stock due to deferred maintenance. The flip side of this prediction is that potential buyers and lenders will favor those markets where information about the neighborhood’s future vitality is readily available. Neighborhood choice is likely to become an even more important component of housing decisions in those markets particularly hard-hit by the Great Recession.

Public policy may be able to play an important role in helping potential homebuyers and lenders make prudent decisions about neighborhood choice, but to do so will require policymakers to tackle difficult decisions about where to target resources. This is a consistent theme in the debate on declining cities in many parts of the world. Government will also have to show short-term successes in order to breed confidence about the potential of long-term recovery. Practical people will want to see evidence of effectiveness after policies are put in place. As such, the “evidence matters” theme espoused by the U.S. Department of Housing and Urban Development (HUD) is a move in the right direction. Two specific policy issues are discussed to highlight these challenges. The first pertains to an aspect of appraisal guidance that calls for an assessment of the neighborhood in which the property is located and, in particular, whether the market is in decline. Improvements in such guidance should be sought. The second is the ambitious neighborhood stabilization programs being supported by HUD. Though each of these policies may become a helpful tool, modifications may help them move us toward a more speedy recovery.

Multiple regulations may need to be re-examined in light of these challenges: forcing lenders to make risky loans in declining markets was certainly not the intent of the Community Reinvestment Act (CRA) and other legislation. Appraisers and lenders who decide that a neighborhood is on the verge of a substantial decline can expect to be challenged on fair lending grounds if the neighborhood contains substantial populations of minority households. Absent strong and compelling evidence, these agents will be susceptible to disparate impact claims. Lenders may have to substantially tighten underwriting standards in all neighborhoods within a metropolitan market particularly hard hit by

a major negative economic shock until it becomes clear which neighborhoods remain viable. Such behavior, though justifiable by a lender seeking to maintain a prudent risk profile, including credit, regulatory, and litigation risk, may in itself hinder recovery efforts for the metros and neighborhoods most in jeopardy. This is an area in which the government may be of help by providing more data, guidelines for forecasts and evidentiary standards. It is likely not a question of whether credit supply will be reduced in these markets, but by how much and by what process.

Lastly, the fundamental problem facing today’s new breed of declining cities and their neighborhoods seems very similar to a problem in many parts of government seeking to manage our economic recovery. That is, investment and lending are seriously hampered by great uncertainty, which in itself hinders the speed of recovery to the “new normal.” Better data and analysis will help everyone become more confident of where we are headed. Data that assess these programs should be made more available to a wide range of institutions committed to objective analyses of the programs. Absent such information, I fear the recovery will be longer and the number of failed neighborhoods greater than they might otherwise be.

The “Great Recession” of 2007 to 2009 has taken a major toll on housing markets in most cities and larger metropolitan areas in all parts of the country. Though the pace and extent of the overall economic recovery of these markets is still far from certain, many places will likely resume growth and fully recover within the next decade. This is almost certainly not to be the case for all metro areas or cities. In fact, a number of large metro areas have been in serious recession and shrinking in size for many years prior to 2007 and for these, a return to their previous sizes may be many years in coming or may not come at all. Even among those metro areas with relatively brighter prospects for growth, certain segments within them may remain well below the peaks in housing prices of the early 2000s.

What is a declining city? Simply put, a declining city is one in which the people have left, but the houses, apartment buildings, offices and storefronts remain. At the extreme, think of a ghost town from the Old West, a town that lost its reason for being. Are there cities or large metro areas in the United States at risk of disappearing back into the desert (or the swamp) today? Probably not, but there are certainly neighborhoods and submarkets within metro areas that have passed a tipping point and have little prospect of returning to anything close to their previous peaks. What are the main factors that generate declining cities? A massive and interdisciplinary body of literature, which is reviewed in Section II, offers a variety of answers to this question. The most common notion of a declining city is a metro area that has experienced substantial declines in population and employment.

Some of these experienced declines because of a loss in their comparative advantage in the production of some key manufacturing product like automobiles or steel. Some cities like Cleveland and Detroit, that fit this traditional notion of a declining city are in the “Rust Belt” region of the United States, but examples of such declining or shrinking cities can be found in other parts of the world like Dresden, Germany. Another type of declining city is generated by natural disasters. The case of New Orleans and Hurricane Katrina is a classic but very recent example. Other potential causes of declining cities have also been offered. Some point to the long-term trend of migration from the colder to the warmer or “Sun Belt” regions of the country. Others highlight the magnetic power of some metro areas such as Silicon Valley in California to attract the brightest and most talented people away from smaller metro areas with less of an advantage as “idea factories.” An issue raised in this paper is whether a new type of declining city may be emerging during the current economic crisis, areas east of Los Angeles and the San Francisco Bay area. These areas were predicated on residents commuting for jobs, low gasoline prices and irrational exuberance about house price growth, but their future viability may be threatened by recent economic events. Each type of declining city offers substantial and unique challenges to agents with a stake in the future of real estate markets within it. These agents include consumers shopping for housing, mortgage lenders seeking to assess the riskiness of real estate lending and governments seeking to develop appropriate regulatory and recovery programs.

The goal of this paper is to offer insights and possible stylized facts about the evolution of the real estate markets in declining cities that may be helpful in making these difficult assessments. The analysis draws upon the experiences of U.S. cities that have experienced severe population and employment declines in the last 40 years as well as others severely affected by the current economic crisis such as Stockton, California.

Attention is focused on three questions:

The answers to these questions are based upon review of the literature and new empirical analysis. Several different sources of data are utilized in order to highlight some of the challenges and opportunities for future or additional empirical work in this field of inquiry.

The following section elaborates on the meaning of declining cities and some of the major explanations offered for their declines, offers empirical evidence to highlight their frequency in the United States over the past 40 years and uses a collection of seven large metro areas to contrast the experiences of traditional Rust Belt cities to some in the Sun Belt that are in the midst of a severe economic decline. The three questions noted above are addressed in Sections III, IV and V, respectively. Each includes a discussion of relevant literature, offers new empirical evidence and provides my best sense of plausible answers to the questions. One particular public policy issue receives considerable attention — appraisal guidance designed to define a declining neighborhood — in the fifth section. The final section offers a summary of the main findings of the paper and argues that the onset of new data sources is a reason to be optimistic about future research on this complex and important topic.

The primary purpose of this section is to expand upon the discussion offered in the introduction regarding various notions of declining cities and to offer empirical evidence to highlight their primary traits. The discussion draws upon some of the literature about declining or “shrinking” cities and highlights several case studies. The case of New Orleans following Hurricane Katrina is treated as a distinct and environmentally generated event that led to unprecedented loss in its population. The discussion also includes a brief review of some other factors raised in the field of economic geography that may be particularly relevant to modern urban life and raises the possibility that a new type of declining city born of the current mortgage and housing crisis may emerge. The section concludes with a review of data regarding urban population patterns in the last 40 years and a closer look at seven metro areas, four of which are in the Rust Belt — Albany, Cleveland, Detroit and Pittsburgh — and three of which are in the Sun Belt — Los Angeles, Miami and Stockton — where the effects of the current recession and housing crisis are particularly acute.

The most common type of declining city is one that suffers a major loss in population owing to a dramatic reduction in its employment base. Economists and geographers have produced substantial research to help understand the reasons for such reductions in the field called “economic geography.” The standard explanation, which has its roots in economic theory going back to David Ricardo, involves a loss in the comparative advantage of a particular city. This comparative advantage may be based on its proximity to water, usefulness as a transportation hub or relatively low wages. With the comparative advantage, industries in this city are able to capture a relatively large share of the national or international market for their product and generate substantial employment among residents of the city. If the comparative advantage vanishes or is greatly diminished due to technological improvements or the development of competitors in other parts of the world, then the comparative advantage can be lost and dramatic declines in employment and population can take place, never to be replaced.

A recent article by Alan Mallach (2010) begins with some examples, specific historical episodes and a compelling narrative to explain the reasons for the existence of the traditional declining city. He cites the economic expansion of the United States in the second half of the 19th century and the first half of the 20th century, which he labels as the “nation’s manufacturing might,” and its substantial decline in the latter part of the 20th century as the primary cause of the traditional declining city. Cities such as Pittsburgh, Detroit, Cleveland and Buffalo and smaller cities like Youngstown, Ohio and Schenectady, New York (the original home of General Electric), are offered as prime examples of declining cities. As a long-time resident of Upstate New York and an economist, I find this story about the consequences of lost comparative advantage familiar and compelling. However, in preparation for this paper, I conducted a review of a long list of case studies about declining cities. Edward Glaeser (2007) offers an excellent summary of the history of one such city in an article entitled “Can Buffalo Ever Come Back?”

A key part of his explanation is the long-time and historically important relationship between Buffalo, New York and the Erie Canal, which was completed in 1825 and allowed Buffalo to prosper as New York City prospered. The presence of the canal allowed for additional types of employment and industrial gains, in addition to the transportation of goods from the Midwest to New York City. For example, Buffalo became a major producer of steel in the early 20th century because it was relatively easy to obtain iron from the Lake Michigan area and turn it into steel. In addition, its proximity to Niagara Falls allowed it to be a substantial generator of electric power. Buffalo was the 13th largest city in America at the onset of the Great Depression. It has since lost 55 percent of its population. Glaeser identifies various explanations for this decline, but his emphasis is upon the losses in its critical areas of comparative advantage. He explains that the key was the loss of its comparative advantage in transportation costs. Growth in rail ended Buffalo’s dominance as a transportation hub. Improvements in the transmission of electricity also reduced its comparative advantage in this industry. Karen Pallagst (2007) offers another insightful discussion in an article entitled “Shrinking Cities in the United States of America: Three Cases, Three Planning Stories.”3

The three cities are Pittsburgh, Youngstown and San Jose, California. Her discussion of San Jose is particularly helpful because it provides a modern day example of a declining city. The primary economic event that led to problems for San Jose was the dot com bust in Silicon Valley at the beginning of the millennium. As a result, the city faced vast losses in its high-tech work force. Pallagst cites a report that the city of San Jose lost 50,000 jobs as a result of the dot com bust. Despite this job loss, its overall population continued to grow due to immigration; however, San Jose was still affected by the loss of so many high paying tech jobs.

The investigation of declining and shrinking cities is not limited to the study of the U.S. experience. Indeed, many countries deal with the issue. Weichmann (2007) “Conversion Strategies under Uncertainty” focuses on post-socialist shrinking cities in Europe. He traces government efforts to manage demographic changes in Dresden, eastern Germany, where the breakdown of the state-directed economy caused economic decline, industrial regression and high unemployment rates. From 1989 to 1999, when the city lost population due to out-migration and decreasing birth rates, the administrative system was still directed towards growth objectives. He makes this point very clearly by presenting the unrealistically high population growth projections utilized by the administrative system during the early 1990s. Then, over the last seven years, the city experienced unexpected growth. Processes of suburbanization have turned into processes of reurbanization, and today in Dresden, areas of shrinkage and decline are in close proximity to prospering and wealthy communities. The strategic challenge is to deal with this patchwork, given that future developments are unpredictable. Other case studies are mentioned in the sections that follow. These case studies and many of the others reviewed communicate some common themes, such as the loss of comparative advantage as a cause of declining cities. They also typically include a substantial emphasis on upgrading the role of government policies. Many champion the notion that some tough choices must be made by government to help revitalize declining cities. These case studies often make another critical point: each place has its own special set of circumstances that make it hard to generalize and difficult to develop a top-down policy for all declining cities.

On rare occasions in the United States, cities have experienced major declines due to an environmental disaster. Galveston, Texas suffered enormous losses in the hurricane of 1900. The major and unprecedented example in recent memory in the United States is, of course, the city of New Orleans, which was powerfully impacted by Hurricane Katrina in 2005. Numerous studies have been conducted of the New Orleans experience. This brief discussion serves as a guide to some of this literature and offers a few statistics from the most recent 2009 American Housing Survey that captures some of the impact on the housing stock in New Orleans. One major study of New Orleans done by the Brookings Institute and entitled “New Orleans at Five” was recently published and its findings are available at the Brookings web site.4

Rather than seek to summarize all of this work, one of the ideas underlying the analysis is described — the notion of a resilient urban economy. A review of the academic literature and case studies by Amy Liu and Allison Plyer (2010) describe factors or characteristics that can increase the ability of a metro area to absorb, minimize or adapt positively to a negative shock and be resilient. They are: i) a strong and diverse regional economy; ii) large shares of skilled and educated workers; iii) wealth; iv) strong social capital; and v) community competence. These become a focus of attention in their ongoing analysis of New Orleans post-Katrina history by Liu and Plyer (2010) and their Brookings colleagues. Other think tanks have offered insights as well and use the New Orleans experience to develop lessons for other cities. One example is a presentation by Anne C. Kubisch (2008) of the Urban

Institute, which draws upon her experiences with recovery operations in New Orleans and what she perceived as the tension between short-term and long-term goals and accomplishments. The lesson she emphasized is this: people need to see short-term progress to increase their faith in the possibility of a long-term recovery. The Nelson Rockefeller Institute of Government produced a series of eight reports including one entitled “Who’s in Charge? Who Should Be? The Role of the Federal Government in Megadisasters: Based on Lessons from Hurricane Katrina,” by Richard P. Nathan and Marc Landy.5

This study argues that there were two disasters. “The first was the immediate crisis created when the hurricanes made landfall. The second was the difficulty various levels of government had in working together to respond to the crisis.” U.S. Department of Housing and Urban Development (HUD) Secretary Shaun Donovan offered testimony on the five-year anniversary of Hurricane Katrina.

He stressed the key role of housing in a complete recovery and the importance of rebuilding the region’s housing stock for families who want to return. The community at one point had lost half its residents, but is now back to over 90 percent of its pre-Katrina population. One of the most important challenges currently faced is vacant buildings and blight across the metropolitan area, where HUD estimates there are 79,000 blighted units today. Soon after this testimony, HUD released results of its 2009 American Housing Survey of New Orleans. The full results are available at HUD’s web site.7

Following are a few takeaways that compare the housing situation in 2004 versus 2009. The total housing stock is down by about 15 percent to its current size of 511,600 units. Renter-occupied housing has taken the biggest hit; it has declined by almost 23 percent to its current size of 142,600 units. The number of housing units in small multifamily structures with five to nine housing units, which are often the homes to low- and moderate-income households, has declined by 32 percent. As a result, and despite the loss in population, the median rent of renter-occupied housing units has increased by 46 percent to its current median value of $876 and is now about 12 percent higher than the median rent for the entire nation. Jay Brinkmann, Chief Economist of the Mortgage Bankers Association (MBA) and Wade D. Ragas (2006) tackled the difficult issue of assessing the cost of rebuilding the housing stock in a 2006 article, which is available at the MBA web site.8

They highlighted two particularly interesting points that hinder recovery. One was the lack of flood insurance by 30,000 or more families that experienced flood damage. Another is the disparate impacts within the New Orleans area. A particular cost reimbursement proposal would cost $9 billion for the entire area and $4 billion for the six hardest hit zip codes.

Beyond these rather clear-cut cases of declining cities, the literature on urbanization and economic geography includes discussions of other factors that can lead to substantial population declines that are difficult to reverse or predict. One of the intellectual leaders in this field is Paul Krugman, who won the 2008 Nobel Prize in Economics for his development and championing of another potential driver of substantial regional economic growth and decline — agglomeration economies. He argues that cities thrive on density, however, if another city can obtain the same or better advantage, then there can be a substantial and irreversible shift from the previous “king” city to the new one. In the context of the United States, this often pertains to growth in western cities relative to the large cities of the Northeast like New York and Boston, that have been the king cities for over two centuries. He places this possibility within the context of the ongoing debate within traditional theory that seeks to explain why developed countries or urban areas tend to specialize in the production of durable goods and developing countries or rural areas tend to specialize in agricultural production. Krugman argues that “traditional theory does not explain why, in reality, world trade is dominated by rich countries trading similar goods with each other. For instance, a country like Sweden exports Volvo and SAAB cars but also imports BMW and Toyota cars.”9

Krugman offers another explanation — agglomeration economies, which are a type of economies of scale. This captures the notion that the fixed costs of production in particular industries and locations can be greatly reduced in areas with substantial research and development. He believes such agglomeration economies are important in explaining the substantial rise in urbanization throughout most parts of the world in the past two centuries. Of course, the flip side of his story is that cities reliant upon such scale economies can suffer great declines if other cities are able to achieve substantial economies of scale by, say, substantial investments in research and development, universities and a well-educated work force. Most importantly, in my view, his theory lays the framework for fast and substantial declines without the prospect of full recovery once, for example, the major cities of the west attain the kinds of agglomeration economies long enjoyed by the East Coast king cities.

Glaeser (1998) lays out a broad description of the costs and benefits of city life and what he considers to be a critical ingredient of urban growth — the benefits of agglomeration economies. While acknowledging that the costs of urban life may increase at some point, he offers some conjectures about the future. He is particularly optimistic about the relatively homogeneous and low density agglomerations of the western United States. Though he does not mention Silicon Valley specifically, this seems to be an example of what he has in mind. These cities offer many of the economic advantages of agglomeration while also reducing the costs of congestion and crime. Ten years later Glaeser and Gottlieb (2009) offered an extensive literature survey and new empirical evidence that again champions the important role agglomeration economies play in the growth of cities. “The largest body of evidence supports the view that cities succeed by spurring the transfer of information” (p. 1023). Their empirical evidence focuses upon the impact of such agglomerations on the growth of cities in the southern and western parts of the United States and the ongoing shift in population toward areas with higher temperatures in January. This story is not so optimistic for the poorer, more heterogeneous, older cities of the East and Midwest, which will have more of a struggle because they will be less likely to be the major sources of innovation.

Another factor also seems likely to affect the relative sizes of Rust Belt and Sun Belt cities — the aging of America. The aging of the “baby boomers” and the growth in the number of retirees seem to have been substantial drivers of migration from Rust Belt to Sun Belt cities in the 1990s and first portion of the 2000s.10 However, interstate migration seems to have slowed down considerably since the onset of the Great Recession. This was likely fueled by diminished wealth and income among the baby boomers due to the decline in home prices and in the stock market, lower interest rates on bonds and lower than anticipated salaries. A recent piece by W. Frey (2009) and his Brookings colleagues offers a number of interesting insights about this issue and an analysis of recent trends. In particular, they say that “Sun Belt states, especially those in the Southeast and Intermountain West, continue to grow faster than those in the Northeast and Midwest. But the recent migration slowdown has led to noticeable reductions in their gains.” Ondrich (2010) addresses another factor affecting the potential outmigration of the baby boomers — the possibility of slower rates of retirement. Indeed, he finds that retirement rates in 2008 are substantially lower than would be predicted by standard models that take into account the declines in wealth associated with recent stock market declines. Retirement rates and associated migration from the Northeast may remain below their 2000 to 2007 rates until the baby boomers recover their lost wealth.

Lastly, another type of declining city may also be emerging — places that grew substantially during the housing boom and are now experiencing unprecedented declines in house prices and increases in foreclosures. In a recent web-based conference hosted by Jesse Abraham of the National Association of Business Economists,11 Celia Chen of Moody gave a presentation entitled “2010: Housing Recuperates.” A key part of her analysis focused on the length of time before a full housing recovery can be expected. One particularly striking graphic highlighted a number of places in California, Nevada, Arizona and Florida where full recovery of the housing market is not expected until 2030.12 Her forecast is based upon the various and negative consequences for the housing markets in these areas stemming from the recent bursting of the house price bubble. Areas in portions of central and eastern California such as Riverside County and Stockton are good examples. These areas were predicated on residents commuting for jobs to Los Angeles or the San Francisco Bay area and overly optimistic views about future house price growth. Sharply higher gas prices and unemployment rates coupled with the crash of their housing markets may threaten the long-term viability of these areas.

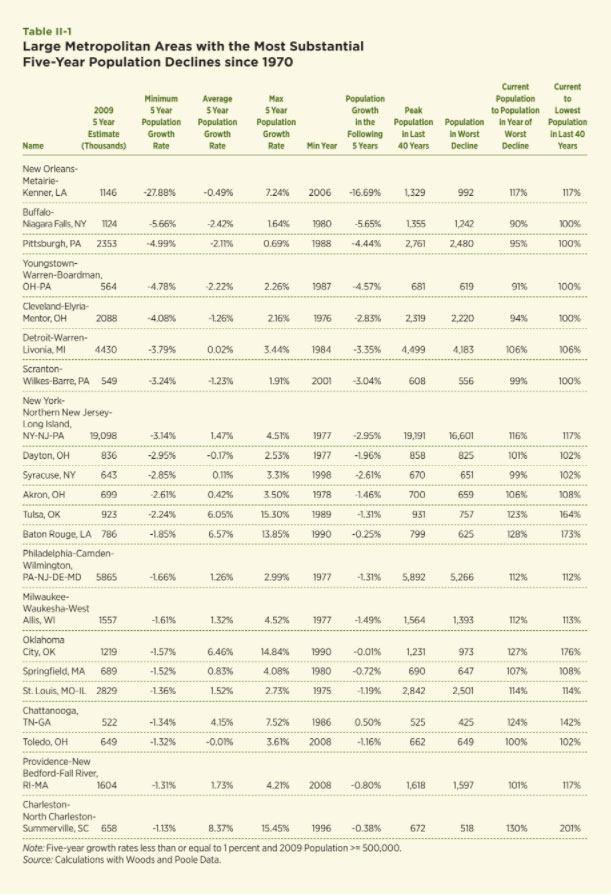

Now attention is focused upon a particular empirical exercise designed to highlight the prevalence of declining cities and their typical recovery patterns within the United States. The exercise involves reviewing the population patterns for 340 MSAs for the period 1970 to 2010. The goal is to generate some insights about the frequency of population declines and typical recovery patterns. For each MSA and each year since 1975, the previous five-year percentage change in population and the subsequent five-year population change are computed. The MSAs are ranked in terms of their largest five-year population declines. 134 of the MSAs experienced a five-year decline of at least one percent since 1970. Table II-1 contains the results for those with a population of at least 500,000. Twenty-two MSAs fit this pattern.

The top of the list by a large amount is the New Orleans MSA, which suffered devastating losses during and after Hurricane Katrina in late August of 2005. 1,836 people were killed and over $80 billion in property damages were recorded. The population in 2005 was 1,312,400; the following year population declined to 992,000. This made the period from 2001 to 2006 the one with the largest five-year percentage decline of –27.88 percent. The current population estimate for 2010 is 17 percent higher than the trough in 2006 but is still about 12 percent short of a recovery to its population at the time of the hurricane. In fact, New Orleans would have easily qualified as a declining city by the criteria used in Table II-1 without Katrina. Population declined by over four percent in the period 1985 to 1990 and had not fully recovered to its 1983 peak population of 1.33 million by the time Katrina hit in 2005. In 2010, this episode alone would have placed it among the top five worst MSA population declines since 1970 among those with populations of at least 500,000.

The next 10 MSAs on the list, with the exception of New York, fit the description of the traditional declining city discussed above. They include Buffalo, Pittsburgh, Youngstown, Cleveland, Detroit and other familiar examples of declining cities in the Rust Belt. Consider Cleveland, which experienced its worst five-year population decline from 1971 to 1976 of –4.08 percent. Its current population is 94 percent of its population at the end of that period (1976) and 90 percent of its peak population in the last 40 years (1971). The story is similar for the other traditional declining cities in this list. The New York MSA is the largest on this list by far and is on the list because of its population declines in the early and mid-1970s. The last year of this period of decline was 1977. Since then population has grown to exceed by a healthy amount its population in the mid-1970s and has experienced positive annual growth each year since the late 1980s.

The bottom part of this list includes some metro areas that might also fit the description of the traditional declining city and some that do not. For example, Oklahoma City is an area that was particularly hard-hit by the oil and savings and loan shocks that hit the Southwest in the early 1980s; however, its population today exceeds its population in the late 1980s by over 27 percent, indicating that a strong recovery has taken place. This case and others on the list highlight a simple fact about U.S. cities: a severe population decrease is not a sufficient condition for persistent and irreversible decline. Overall, this empirical exercise confirms a list of usual suspects for the label “declining city” and the fact that population growth for them, even during the relatively prosperous years since 1970, is much slower than in much of the rest of the nation and insufficient to return them to their previous peaks. On the other hand, keep in mind that this list only contains six areas that are still below their population levels as of the beginning of the period of decline, which is a small fraction of the 340-plus metro areas from which this list was compiled. That is, the classic experience of the declining city, using relatively large metro areas with populations of at least 500,000, is relatively rare in the last 40 years. Recoveries can and do happen.

A similar analysis of five-year changes in the number of households was also conducted. The resulting list includes many of the same metro areas as the one based upon population patterns, though two more Upstate New York metro areas are now on the list, Syracuse and Albany. New Orleans and Buffalo again top the list using these criteria. Another interesting result of the analysis of households is how few metro areas actually experienced declines in their household populations even when their total populations declined substantially. In fact, all but New Orleans and Youngstown have populations above their previous peak since 1970 and all have household populations above the number at the end of the worst five-year period of decline. Hence, the number of households recovers more quickly and more completely than population. This likely reflects the possibility that household size declines when there are ample housing vacancies, which presumably lowers housing costs for those who remain. It may also reflect a point raised by many authors, including Glaeser; that is, the ample supply of vacant housing in declining cities likely attracts new migrants with relatively lower incomes who are attracted to the lower cost housing.

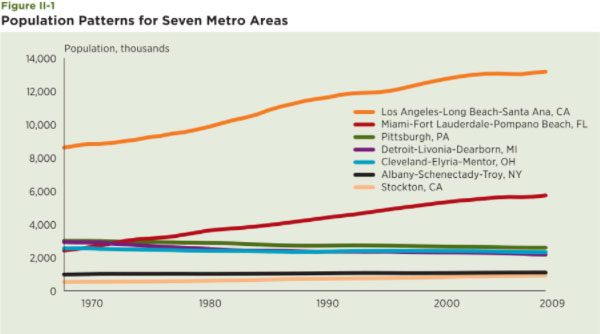

Seven metro areas are selected for scrutiny in order to provide a closer look at these various notions of a declining city. Four encompass cities and urban areas that fit the notion of the traditional declining city from the Rust Belt: Albany-Schenectady-Troy, New York; Cleveland-Elyria-Mentor, Ohio; Detroit-Warren-Livonia, Michigan; and Pittsburgh, Pennsylvania. The other three are among the fastest-growing metro areas in the country over the past 30 years. Two are very large: Los Angeles-Santa Ana, California and Miami-Fort Lauderdale-Miami Beach, Florida. The third is Stockton, California. These areas encompass 11 smaller metro areas and 29 counties. These are used throughout the paper to highlight differences in their growth patterns over the past 40 years and their experiences during the boom and bust period of the 2000s.

A comparison of these areas begins with a look at their population patterns since 1969 (see Figure II-1). The top two lines refer to Los Angeles and Miami, both of which increased substantially in size in the past 40 years. Los Angeles increased by 54 percent, Miami increased by 148 percent. Stockton is the line at the bottom. Though relatively small in comparison to the other metro areas in this group, it has grown by 136 percent since 1969. Contrast these patterns to the declining metro areas. The Cleveland, Detroit and Pittsburgh metro areas all declined in population during this period. Cleveland declined by nine percent, Detroit by 27 percent and Pittsburgh by 15 percent. The Albany metro area grew by 15 percent during this period but is included because it includes one of the best examples of a traditional declining city — Schenectady, New York. The city of Schenectady had a population of over 90,000 people in 1950, 78,000 in 1970 and just over 61,000 today.

A look at employment trends among these seven metro areas highlights an important point: population and employment are correlated, but not perfectly (see Figure II-2). While Detroit experienced nearly identical percentage declines in population and employment of about 27 percent, the other declining metro areas experienced gains in employment. Cleveland and Pittsburgh experienced positive employment growth rates of 16 and 26 percent, respectively. Employment also grew much more rapidly than population in Los Angeles (91 percent) and Miami (223 percent). Stockton’s large population growth over this period was matched almost exactly by its employment growth.

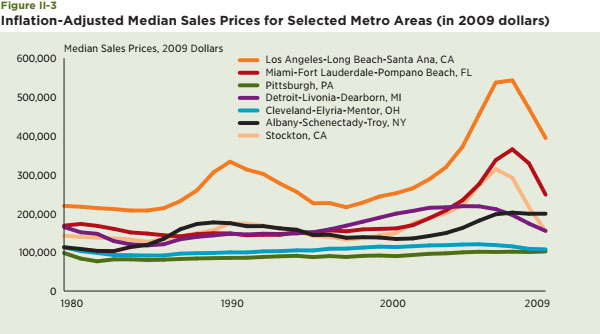

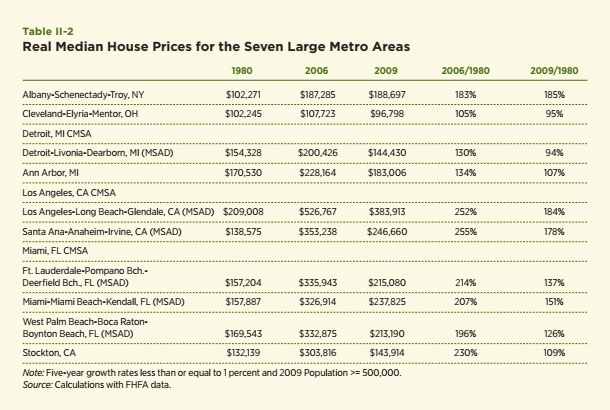

The last of this initial set of comparisons among the large metro areas offered in this section focuses upon house prices. These are available separately for each of the 11 smaller metro areas among the seven larger urban areas. Figure II-3 contains the median sales prices from 1980 through 2009 adjusted for inflation and are stated in terms of 2009 dollars.13 Selected values are contained in Table II-2.

The levels of house prices and their growth rates varied substantially among these metro areas in the last 30 years. This is especially true if attention is focused upon the values at the peak of the recent house price boom, 2006, relative to values in 1980 (see Table II-2). For example, real house prices in Los Angeles were 285 percent higher in 2006 than in 1980 and even after recent declines, stand at 185 percent of their 1980 values. In contrast, real house prices in Cleveland and Detroit are now five percent lower than in 1980, though they did briefly exceed the 1980 values for a period in the mid-2000s. The case of Stockton is particularly striking. The median house price in Stockton grew by 230 percent from 1980 to 2006, but is just nine percent higher today than in 1980 and about equal to the median house price in Detroit. Clearly, the Rust Belt cities did not experience the growth the Sun Belt cities did; but they also did not experience the same degree of decline.

This section discusses and presents evidence about the pattern of real estate values in metro areas that have experienced substantial and persistent declines in population and employment. A powerful narrative and strong empirical evidence suggest that house prices in such cities experience steep declines during the period of population and employment decline; furthermore, the recovery in house prices is very slow and incomplete. The intuition underlying this story is relatively simple and consistent with basic models of supply and demand: people move; houses, apartment buildings, offices and shopping malls do not. As a result, declining cities can expect to experience a steep decline in the demand for existing housing, which leads to much lower house prices given that the stock of existing housing is relatively fixed. Full recovery of house prices in such an environment requires either a reduction in the stock of housing or a resurgence in the size of the population.

The basis for this prediction has been examined in a large theoretical and empirical body of literature about the price elasticity of the supply of housing. The literature typically seeks to explain the response of house prices to shocks stemming from an increase in the demand for housing, which can be generated by increases in the main drivers of housing demand: population, household income and interest rates. Generally, the price of new housing is relatively elastic; that is, growth in demand leads to substantial increases in housing supply and relatively modest increases in house prices. Builders respond to a positive gap between the market price of housing and the cost of construction by increasing their production of new housing. As a result, substantial and prolonged above-normal rates of house price growth due to increases in demand are not the norm as long as space for additional housing is available and the regulatory environment is supportive of additional housing. If either of these conditions is not satisfied, then expansion of the supply of housing is inhibited and substantial and sustained price increases are possible.

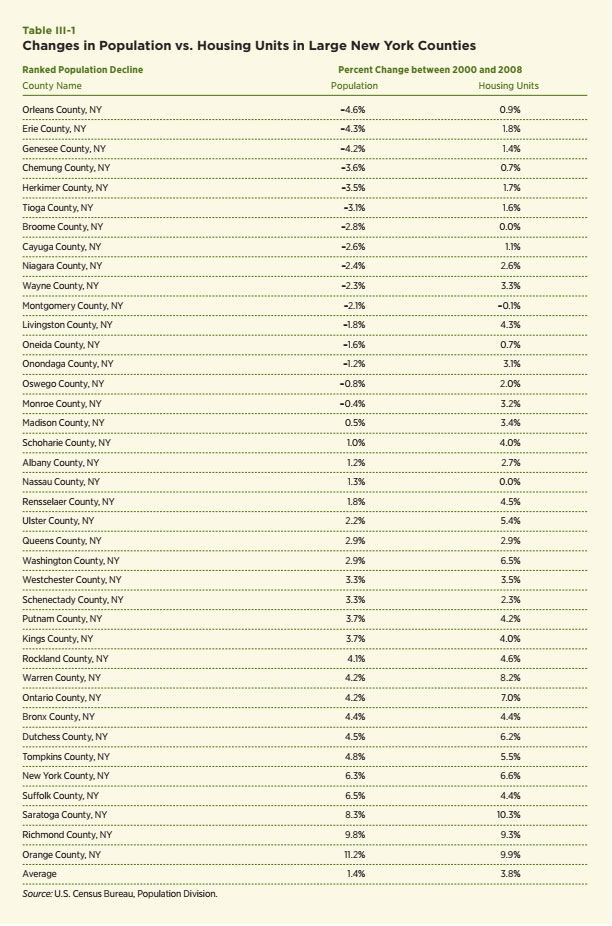

This study focuses on markets in which demand is in a state of persistent decline. What happens to house prices in these markets? Glaeser and Gyourko (2005) present both a comprehensive narrative and compelling empirical evidence that house prices in declining cities can be expected to decline sharply and recover slowly in their study of urban decline and urban housing. At the core of their view is a “kinked” supply curve, which is relatively flat (elastic) for additions to the housing stock and relatively steep (inelastic) for reductions in demand. In such an environment, persistent declines in demand generate substantial declines in prices. They offer two key pieces of empirical evidence. The first examines patterns of population change and demonstrates that population declines in cities tend to be persistent or lead to further population declines for a considerable period of time. The second shows that house price changes differ substantially among cities in the midst of a period of substantial and persistent population decline versus cities that experience population growth. Their empirical evidence involves the examination of 10-year changes in house prices for 321 city clusters using Census data for 1970, 1980 and 2000. The focus is upon the response of population and house price growth for each 10-year period as a function of the growth in the population of these cities. Strong empirical evidence of an asymmetric effect of population growth upon house price growth is presented. In particular, a decline in population growth by one percent leads to nearly a two-percentage point drop in real house prices over the decade. In contrast, real house prices grow by only about 0.23 percent per one-percent growth in population growth among growing cities. That is, the price decline over a 10-year period stemming from a one-percent decline in population is about nine times higher than the increase in house prices for a one-percent increase in population for the same period. Additional empirical evidence is presented in this section that both supports and expands upon the story told by Glaeser and Gyourko. The first exhibit is a simple examination of the correlation between growth in the size of the housing stock and growth in population for counties in New York State for the period 2000 to 2008 (see Table III-1). The counties are ranked by the size of population declines between 2000 and 2008. Sixteen counties experienced population declines during this period. Among this group, only one experienced a decline in the housing stock, and this was only –.01 percent for Montgomery County, which is a relatively rural county in the Albany-Schenectady MSA. Clearly, the people moved but the houses are still there.

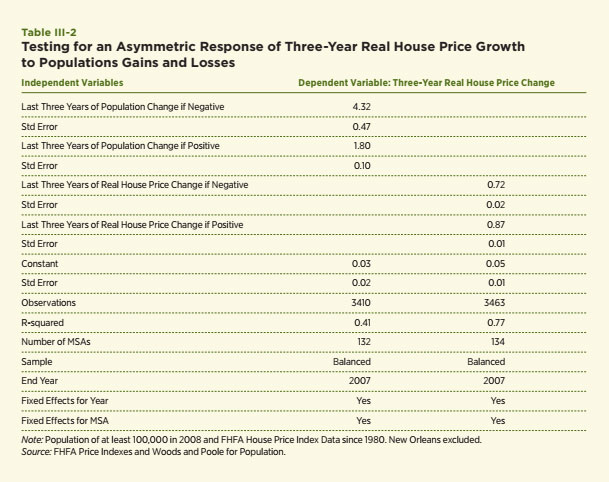

The second piece of empirical evidence focuses specifically on the relationship between real house price growth and changes in population growth. It mirrors the analysis of Glaeser and Gyourko, but uses a different and potentially richer data set on house prices. Real house price growth is measured using the Federal Housing Finance Agency (FHFA) house price indexes for metropolitan areas and population data from Woods and Poole.15, 16 The estimation uses data on 132 metro areas with population in 2008 of at least 100,000 people and with FHFA price indexes that begin in 1980 or earlier; the total number of observations is 3,410.17 The data include years 1980 to 2007. The dependent variable is the most recent three-year percentage change in real house prices. The independent variables include the most recent three-year percentage losses in population or gains in population. The measure of population loss is either a negative number or 0; similarly, the measure of population gain is either positive or zero. This allows the model to capture the asymmetric impact of population gains versus losses. The model also includes fixed effects for both the metro area and each year of data in order to control for all of the other variables that impact house prices. The results and key statistics are contained in the first column of Table III-2.

The results strongly confirm the basic hypothesis and the Glaeser and Gyourko results. The key coefficients are now 4.32 for a population loss and 1.80 for a population gain. Thus a one-percent population decrease is estimated to reduce house prices by 4.32 percent over a three-year period whereas a one-percent population increase is estimated to increase house price growth by only 1.80 percent. This asymmetric result is consistent with the basic narrative that people move faster than real estate.

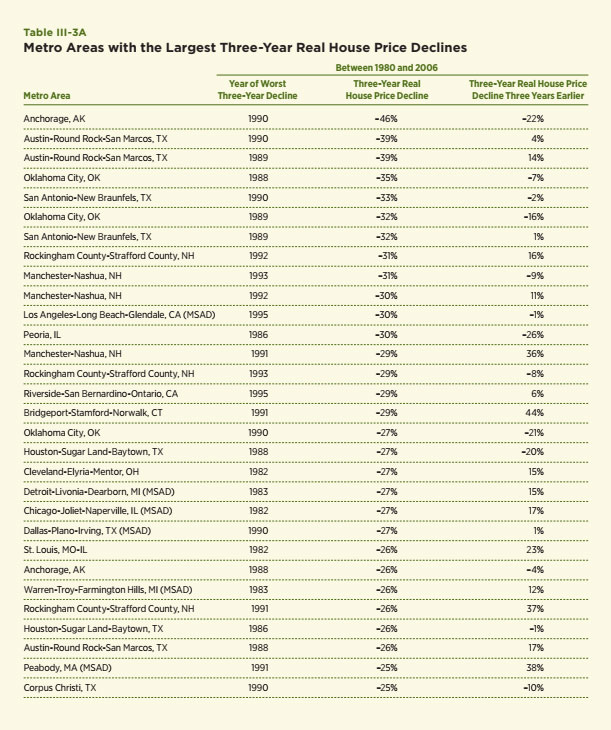

Now attention is turned to a different but related question: Does a period of substantial house price decline tend to be followed by another period of declining house prices? This is almost an inverse of a question addressed in a Federal Deposit Insurance Corporation (FDIC) study by Angell and Norman (2005) entitled “U.S. House Prices: Does a Bust Always Follow a Boom”? They conclude that a bust does not typically follow a boom using FHFA house price index data for the period 1979 to 2003. The most typical outcome after a period of substantial house price growth is a period of relatively flat house price growth. I address a similar but different question: Does a house price bust always follow a house price bust? The question is explored by estimating a regression equation similar to the one reported in Column 1 of Table III-3AB and using the same data to examine how three-year real price changes as functions of the most recent and lagged three-year real house price declines. The specification includes fixed effects for each metro area and each year in the sample. These results are contained in Column 2 of Table III-3AB.

The coefficients of the two lagged values of house price change do not exhibit the same asymmetry as found with population gains and losses. The coefficients on the two lagged values of real house price change are 0.72, if the lagged price change was negative and 0.87, if the lagged price change was positive. In fact, they suggest that the impact of a lagged price increase is actually larger than that for a lagged price decline.

Here is a potential explanation of these results and why we find an asymmetric response in the case of lagged population growth but not lagged house price growth. House price declines can be generated by a variety of variables that affect housing demand. These include increases in interest rates, tighter credit and lower average household incomes. In such cases, house prices can be expected to decrease, all else equal; however, declines in these nonpopulation factors have not typically been as persistent as the population decreases associated with declining cities so well articulated and documented by Glaeser and Gyourko and confirmed by the evidence offered in this paper. If so, house price declines generated by reductions in, say, average household income or increases in interest rates will be less asymmetric since reductions in household income or increases in interest rates do not necessarily bring about declines in population and a build up of excess housing stock.

In fact, a review of the experiences of the metro areas with the largest declines in house prices supports this view and also highlights the uniqueness of the last few years. Three-year changes in real house prices were computed for each of the 384 metro areas for which FHFA data are available.18 The left portion of Table III-3AB lists the 30 metro areas with the largest three-year declines in real house prices using data through 2008. All of these had declines of at least 25 percent over a three-year period. The largest decline was 46 percent for Anchorage, Alaska for the period 1988 to 1990. Note that two of those on the list fit the notion of a traditional declining city: Warren, Michigan, which is a metro area within the larger Detroit metro area and Detroit itself. The rest are heavily concentrated in the Sun Belt and, in particular, the Southwest. These include many that were particularly hard-hit by the oil and savings and loan crises of the 1980s, such as Austin, Oklahoma City, San Antonio and Houston. In fact, the experiences of this part of the country formed the worst regional house price decline in the United States until the current crisis and formed the basis of the house price stress test scenario used to evaluate the credit risk for the portfolios of Fannie Mae and Freddie Mac. However, these places do not fit the notion of the traditional declining city and the declines were more likely driven by relatively temporary declines in household incomes and rising interest rates during this period, rather than by persistent population declines. Most importantly, 17 of these metro areas had positive growth in the previous three-year period and the average growth rate in the prior three years was five percent; hence, a substantial period of house price decline does not appear to be a strong predictor of future house price declines. In addition, many of the places have recovered rather nicely since the late 1980s in contrast to the experiences of traditional declining cities. I view this as consistent with the narrative offered in the previous paragraph: house price declines are not necessarily or even usually self-perpetuating, rather they depend upon what caused them. If the cause is a persistent decline in population and employment that leaves a substantial excess supply, then a persistent decline in house prices can be expected. If, however, the causes of the decline are related to temporary declines in other drivers of housing demand, then house prices do seem able to recover with time in most areas..

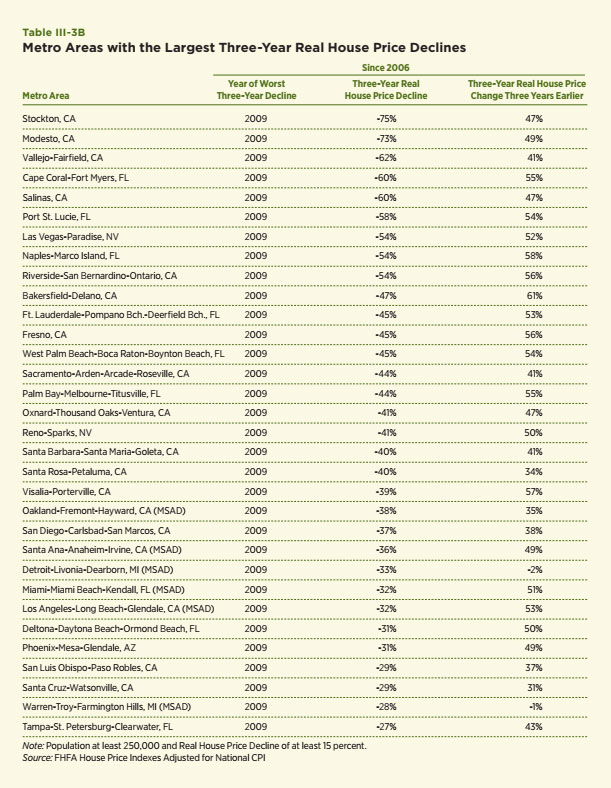

Now consider another lesson of this empirical exercise. When the list of metro areas is compiled using data through 2009 (see Table III-3B), the metro areas with the worst three-year house price declines are dominated by the period 2007 to 2009. Stockton and Merced, its nearby neighbor in the eastern portion of California, top the list with real price declines of nearly 75 percent. Most of the others on the list are metro areas in the Sun Belt. The only traditional declining cities on the list are, again, Detroit and Warren. Hence, the current housing crisis leads to a completely different list with declines that surpass the competition for the worst house price declines in the United States since 1980. Note, too, that the price declines in 2007 to 2009 for all but the two declining cities were preceded by a period of substantial house price increases in 2005 to 2007. The simple average of the price increases for this list in the period 2006 to 2009 was 45 percent. The simple average of the declines for the period 2007 to 2009 was almost the exact opposite, –44 percent. What we do not know at this time is whether house prices in these areas will soon or ever recover. History is still being written, though some like Celia Chen, who uses the models of Economy.com, do not appear to be optimistic about the pace of recovery for many of these areas.

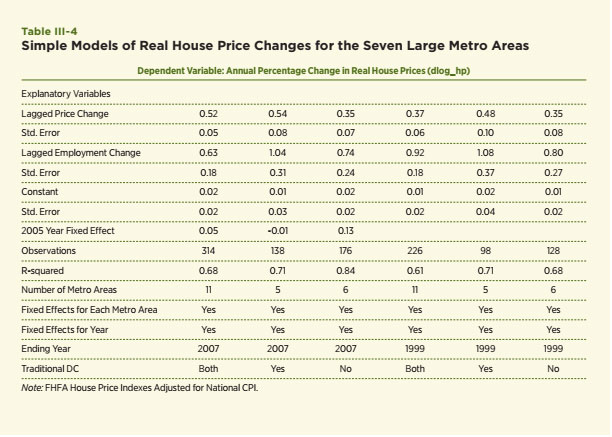

Some insights are sought by estimating a simple house price model for the metro areas discussed earlier. The model explains the growth rate in real house prices as a function of lagged house price growth, lagged employment growth and a set of fixed effects for each metro area and year. The 11 metro areas included in Table II-2 are the focus of attention. The model is estimated for all 11 using data through 2007 and then separately for the traditional declining cities and the Sun Belt cities. These three specifications are also used to estimate a model using data through 1999 to capture any substantial changes in the model since 2000. The estimation results are

contained in Table III-4.

First, I am struck by the similarity of the estimated coefficients on the lagged values of house price and employment growth. The declining metro areas appear to be modestly more responsive to real factors as captured by the coefficients for lagged employment growth (1.04 versus 0.74). The lagged house price appreciation is relatively more important in the declining metro areas (0.54 versus 0.35), but the differences are not large and both are substantially below unity. Coefficient estimates closer to 1.0 (unity) would be expected if recent house price growth by itself was a strong predictor of the future. Estimating the model using data prior to 2000 and the core years of the house price boom of the early and mid-2000s generates similar estimates.

Second, the most dramatic differences show up in the fixed effects for each year of data. In particular, the estimates of the fixed-year effects for the Sun Belt metro areas far exceed those for the declining metro areas in the early 2000s. For example, the fixed effect for the Sun Belt is 12.7 percent for 2005 versus –0.7 percent for the declining cities in this year. Clearly, something very different was happening in the Sun Belt that was quite out of the ordinary and, perhaps, unlikely to crop up in the near future. My inclination is to label this a sign of inflated expectations or the irrational exuberance in the Sun Belt in the early 2000s, though there were clearly other factors, such as the increased availability of mortgage credit and substantial immigration, involved.19 Otherwise, I was struck by the similarity of the core estimates for these two groups of seemingly very different metro areas with vastly different experiences during the past 30 years.

The key points of the analysis in this section are as follows. First, substantial price declines can be expected to occur at the MSA level in places that suffer substantial and persistent declines in population

and employment (see Table III-2). Second, the simple fact of a period of substantial house price decline

is not necessarily a signal of future price declines and a long and incomplete recovery (see Table III-

3). Third, estimates of a relatively simple econometric model of house price growth for the smaller

set of Rust Belt and Sun Belt metro areas reveal one particularly striking difference — a dramatically larger estimate of fixed effects for the early part of the 2000s, especially 2005. Overall, these results are consistent with the view that substantial price declines can be driven by a variety of factors that affect demand, not just population or employment. If these other factors are not persistently in decline, then house price declines in these areas need not be persistent either. For example, a return to more normal house price expectations and more normal access to mortgage credit relative to the early 2000s can be expected to reduce housing demand and house prices relative to the peak years of irrational exuberance. Once the “new normal” for these variables is reached, housing demand may well return to a positive growth rate and house prices will begin to recover. Of course, we are still in the midst of the current mortgage crisis and more time is needed to discover what that new normal will be in those areas particularly hard-hit during this crisis and when it will occur.

Do some neighborhoods within a declining city decline more than others? In particular, do some neighborhoods suffer extreme declines that threaten their long term viability? Such situations are sometimes called “tipping points,” which refers to situations in which a particular organization or neighborhood faces circumstances so severe it becomes no longer viable. What I have in mind is somewhat like the decisions being made within many Catholic dioceses about which particular parishes to close down due to a shortage of priests and aging and diminished congregations. This particular example is apparent in many declining cities within New York.

Much has been written about various patterns of intra-metropolitan decline. Some has focused upon the decline of the central city of a large metropolitan area relative to its suburban areas.20 Another large body of literature exists that features case studies of specific neighborhood declines and the challenge of identifying the key traits of a viable neighborhood. This approach is especially common within the field of urban and regional planning. The analysis offered in this section seeks to supplement these important contributions in two ways. First, the primary focus is upon smaller areas within the metro area such as Census tracts and zip codes. Second, attention is focused upon several specific metrics of real estate activity that are available for a large number of metro areas and offer the opportunity to provide some insight into the dynamics underlying neighborhood change during the current crisis in the mortgage and housing market.

Throughout the section, emphasis is upon the use of the metrics to describe and document widely disparate intra-metropolitan impacts. The possibility of widely disparate neighborhood outcomes within a declining city is especially important to households and businesses seeking to make long-term real estate investments and particularly important to lenders seeking to build a successful

mortgage lending business. All else equal, lenders prefer an environment with a relatively narrow set of possible future outcomes because the larger the dispersion of possible future outcomes for a particular neighborhood, the greater the risk for such investments and lending. Take for example a lender seeking to assess the mortgage credit risk of a loan in a declining city. The riskiness is directly related to the possible dispersion of outcomes. A situation in which 80 percent of the neighborhoods survive and return to normal activity within a fairly short period but 20 percent of the areas become no longer viable may be much riskier than a lending business targeted to an area in which the risk of a tipping point is less than five percent.

A Mortgage Banking magazine article by Follain and Sklarz (2005) may help explain this point. In that paper, we sought to highlight the additional credit risk of a metropolitan area in the midst of a house price bubble versus one experiencing a more normal rate of growth in housing prices. Those areas in the midst of a potential bubble faced greater probabilities of substantial declines in house prices than areas experiencing normal growth. Prudent lenders would seek to incorporate this additional source of credit risk into their pricing; hence, we titled our article “Pricing Market Specific Bubbles” and provided estimates of the additional credit risk spread needed to account for the additional credit risk due to the potential of a bubble bust. Essentially, the same kind of question or analysis might apply to neighborhoods within a metro area. If some face a disproportionate risk of a steep decline, then prudent risk management would seek to incorporate this finding into pricing and business models. Prudent risk management must also take into account the regulatory and litigation risk involved in such analysis, since fair lending experts typically warn lenders to avoid establishing lending criteria below the metro level for fear of being accused of redlining.

Of course, the possibility of a disproportionate impact among neighborhoods within a declining city is a critical question for government as well. A recent article by Mallach (2010) does an excellent job of highlighting what is at stake and offers his views about what government can do better. He states his major theme as this: “How these cities acknowledge the reality of being a smaller city, reconfigure their physical environment, reuse surplus land and buildings, and target their resources to capitalize on their assets will likely determine whether they will continue to decline, or will achieve vitality as smaller but stronger cities.” Though his focus is primarily upon cities rather than neighborhoods, implicit in his analysis is that some neighborhoods may not return to anything near their pre-decline levels. He offers a variety of potential governmental remedies to help, most of which involve putting more focus upon a smaller number of targeted programs that recognize that all neighborhoods do not face the same future prospects.

Neighborhoods can be and are characterized in a large number of ways. Some of the more obvious descriptors involve school quality, crime, resident incomes and access to transportation and jobs, but there are many other possible candidates. Hence, a metric for neighborhood decline requires both a choice of the descriptors of neighborhood decline and data for the chosen variables.

One particularly interesting case study of Flint, Michigan by Hollander (2010) offers great insight into the challenges of choosing a metric and a specific suggestion for a declining city. He argues that, “Conventional community development and planning responses have looked to reverse the process of

depopulation almost universally, with little attention paid to how neighborhoods physically change when they lose population.” He suggests, “an approach to study the physical changes of depopulating neighborhoods in a novel way. The approach considers how population decline creates different physical impacts (more or less housing abandonment, for example) across different neighborhoods. Data presented from a detailed case study of Flint, Michigan, illustrate that population decline can be more painful in some neighborhoods than in others, suggesting that this article’s proposed approach may be useful in implementing smart decline.” What is particularly striking about the approach is the enormous amount of qualitative steps taken to generate his suggested metric — housing units per acre. These included examining Census data, ground observations of neighborhood conditions and interviews with local officials, residents and community leaders. The efforts were largely confined to three neighborhoods within Flint. Though this study is very insightful and compelling, Hollander readily admits that it is difficult to generalize from this particular case study to all neighborhoods and all declining cities, but he surely and effectively champions the need for measureable criteria in order to develop sound public policy remedies.

The research in this paper considered a variety of neighborhood metrics and ultimately settled on four: vacancy rates, house prices, the number of housing sales and the value of the single-family housing stock. Each is selected because they represent plausible measures of real estate activity at the neighborhood level and because data are available to measure them. Three sources of data are used for these variables and the discussion of the empirical evidence is organized around each data source.

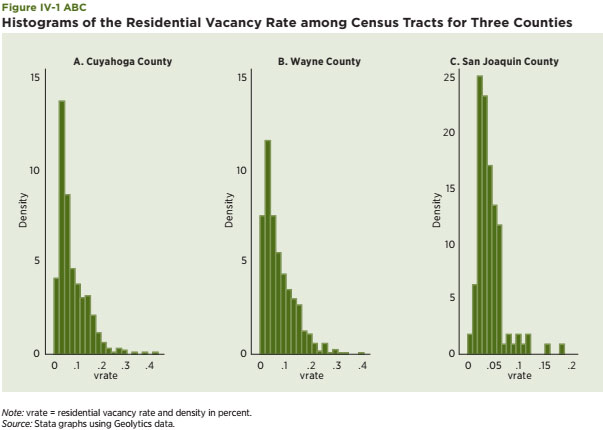

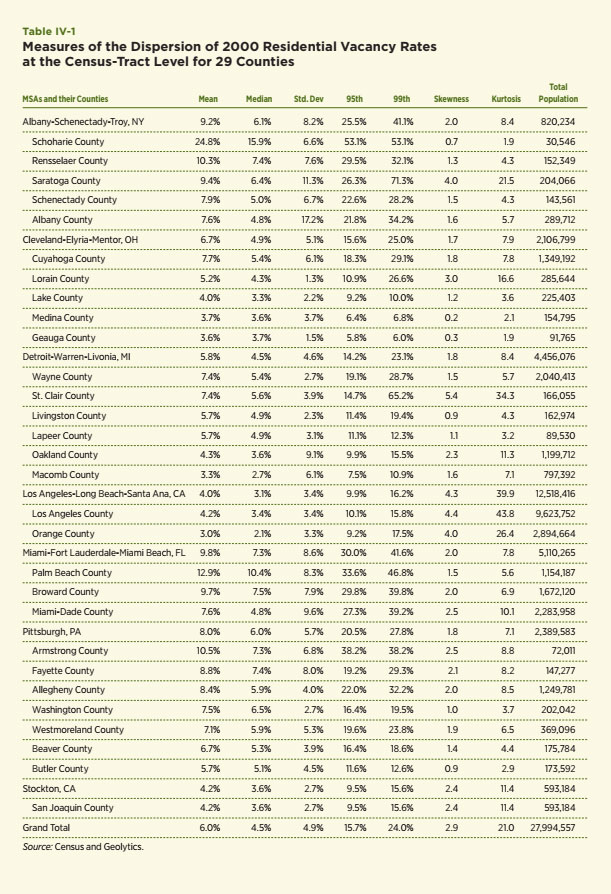

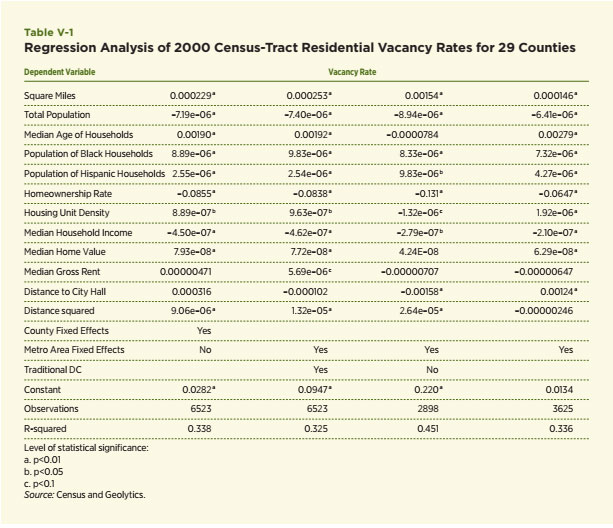

The Census-generated vacancy rate measures whether a housing unit was occupied at the time of the Census interview. It seems to capture a core notion of neighborhood decline and the explanations offered in the previous section about why house prices decrease in the traditional declining city — people move more quickly than housing units, a pattern that generates vacant housing units. It also captures the potential of extreme outcomes when all or most housing is vacant and the neighborhood is no longer considered viable. The source of information for this part of the empirical analysis is the information provided and compiled at the Census-tract level. This data product includes hundreds of variables for places all over the country, along with mapping capabilities, which are helpful in highlighting disparate neighborhood impacts. The vacancy rate is computed as the ratio of the total number of vacant housing units in a Census tract relative to the total number of housing units. The study used year 2000 data. Census-tract data for the seven metro areas discussed in previous sections are used for the analysis.21 These are chosen in order to have a mixture of traditional declining cities and Sun Belt cities particularly hard-hit by the current housing crisis. First, histograms of the distribution of the vacancy rate at the Census-tract level are generated for three counties: Cuyahoga, in the Cleveland metro area, Wayne County in the Detroit metro area, and San Joaquin, in the Stockton metro area (see Figure IV-1 A, B and C).22 They are designed to capture the dispersion of the vacancy rate in 2000 and highlight potential differences among these metro areas at that time. The key takeaway is that the tails of the vacancy rate distribution for Cuyahoga and Wayne Counties, both traditional declining cities, are much fatter and tilted toward larger values relative to that for San Joaquin County, which is the only county in the Stockton metro area and is the representative Sun Belt city in this group. Note, also, that vacancy rates in 2000 were also lower and more tightly bunched in San Joaquin County than in Cuyahoga and Wayne Counties.

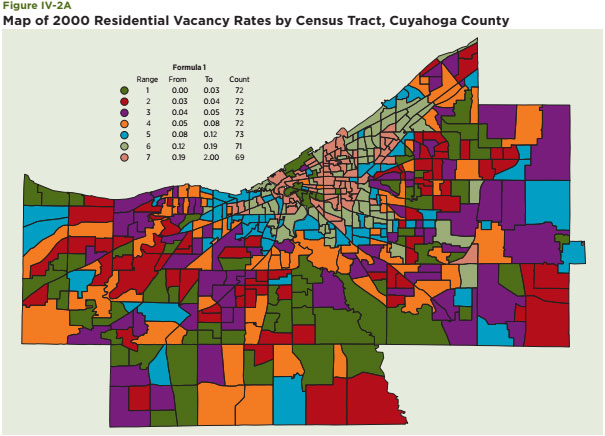

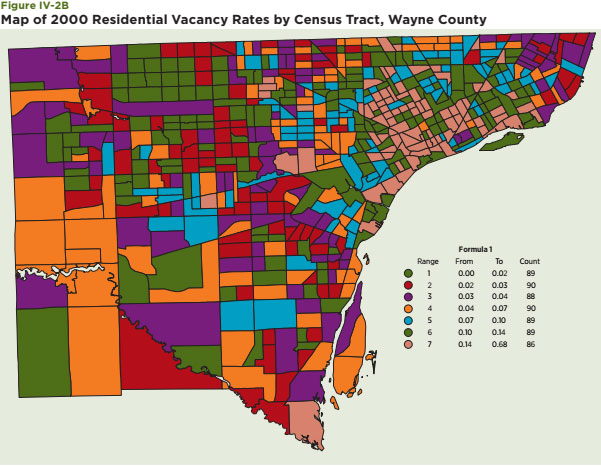

Second, maps of the distribution of the vacancy rate among all Census tracts within Cuyahoga and Wayne Counties are also presented to highlight the substantial dispersion of vacancies within these areas (Figure IV-2A and B).23 The sharp contrast in the areas in the upper center part of the map of Cuyahoga, which are generally within the city of Cleveland, captures this dispersion nicely. For the case of Wayne County, vacancy rates are highest in the northeastern portion of the map, which includes many Census tracts within the city of Detroit. Though vacancy rates are typically lower in the Census tracts outside the city to the west, examples of Census tracts with low vacancy rates are also apparent within the city of Detroit.

Maps are a helpful way to view the dispersion, but predictive methods benefit greatly from statistical measures of dispersion. The following generates a wide set of statistical measures of the vacancy rate distribution to capture the extent and character of the dispersion of vacancy rates within each county and among the 29 counties selected for scrutiny. They include the standard measures: mean, median and the standard deviation of the distributions, which are most helpful when distributions are rather stable and normally distributed. I also include two measures that shed light on the extreme values of the vacancy rate distribution: the 95th and 99th percentile values of the vacancy rate for each county. Lastly, they include two other measures specifically geared to capture whether a distribution is skewed in one direction or another from the mean — skewness — and whether the distribution is particularly narrow or peaked relative to the normal distribution — kurtosis. The larger the skewness measures, the more the distribution is tilted toward relatively large values of the vacancy rate. The larger the kurtosis measure, the more peaked and the tighter the distribution of vacancy rates around the mean value. Values in excess of three indicate that the distribution is less peaked or flatter than the standard normal distribution.

A few patterns emerge from this exercise, the results of which are contained in Table IV-1. First, as expected, the mean, median and standard deviations are lower in Los Angeles and Stockton — two growing metro areas at that time — than in the Albany, Cleveland, Detroit and Pittsburgh metro areas, which is expected. Second, the vacancy rates were also quite high in Miami. This highlights a potential problem with the vacancy rate as measured by the Census — its failure to distinguish seasonal vacancies related to tourists and second homes. Third, the extreme measures tend to be higher in many of the primarily urban counties within Cleveland, Detroit, Pittsburgh and Albany; however, the most extreme values are often in the relatively rural areas of each larger metropolitan area. Schoharie, New York is the best example of this point. Fourth, larger values of skewness, which indicate the potential tipping of the vacancy rate distribution toward larger values, are not confined to the counties associated with traditional declining cities. Similarly, large values of kurtosis, which would represent a relatively tight and sharply peaked distribution, are found for Los Angeles, Stockton and some of the suburban counties, but again, the pattern is affected by relatively rural areas and those with seasonal housing.

Overall, this exercise with residential vacancy rates from the 2000 Census offers good insights about the extent of their dispersion within declining versus Sun Belt cities. The analysis surely seems to confirm that their distributions at the Census-tract level depict a wide range of outcomes with what we would typically consider extreme values. A simple normal distribution of outcomes within these counties does not seem to be appropriate for many or even most counties. Even among the Sun Belt areas, there are examples of Census tracts with substantial vacancy rates. Nonetheless, this particular vacancy rate measure has several limitations. It is available only during Census years and only for residential units. Also, as is demonstrated in the next section, its failure to take into account the duration of vacancies seems a particularly important limitation since a substantial number of long- term vacancies is likely to be a hallmark measure of a neighborhood nearing a tipping point. The next data source to be considered on vacancy rates — the United States Postal Service (USPS) Vacancy Survey — offers the opportunity to improve the value of the vacancy rate as a metric for dispersion and, in particular, the identification of extreme outcomes.

The USPS has entered into an agreement with HUD to provide a “real-time, attribute-rich, parcel-based data system” to help monitor and address the critical issue of neighborhoods with substantial numbers of vacant and abandoned properties. The output of this agreement is a Metropolitan Area Quarterly Vacancy Report. Each quarter HUD receives Address Management System (AMS) ZIP+4 extracts of addresses identified by USPS carriers as having been “vacant” or “no-stat” and aggregates this data to the Census-tract level for release on HUD’s Office of Policy Development and Research web site. The USPS Vacancy Survey has been available for over 60,000 Census tracts on a quarterly basis from 2005 through 2010:Q2.

There are three particularly attractive features of these data relative to the Census-measured vacancy rates. First, they offer measures of the duration of vacancies. Second, vacancy rate information is available for both residential and business addresses. Third, they provide an excellent opportunity to study the evolving impacts during the current crisis. Each of these features is exploited to provide insights about the dispersion of vacancy rate changes within markets experiencing substantial declines in their housing markets.

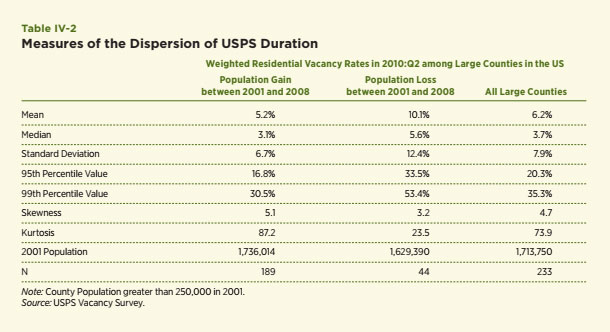

The USPS survey provides information about the total number of residential addresses and the number of vacant addresses, which allows computation of a Census-like measure of the vacancy rate, but the Census measure only indicates whether the property was vacant at the sampling date. The USPS measure also offers information about the average number of days that the units are vacant. This permits the computation of a more general and robust measure of vacancies. The definition used in this section (VR_days) is as follows: VR_days = number of vacant units × average number of days vacant / (365 × number of addresses). As such, VR_days measures the fraction of days that the residential housing stock was vacant during a year relative to 100 percent occupancy.25 This measure generally provides much higher estimates of vacancies than the Census measures. For example, the average Census vacancy rate among the 64,891 Census tracts in the 2010:Q2 USPS was 4.2 percent whereas the duration-weighted vacancy rate was 7.0 percent, which is more than 68 percent higher. We utilize this enhanced measure of vacancies to highlight differences in the various statistical measures of dispersion noted above. One comparison focuses upon the dispersion of VR_days among 233 counties with a population of at least 250,000 people in 2000. The distinction is made between those that grew in population between 2000 and 2008 (189 counties) and those that declined in population (see Table IV-2).

These results demonstrate a much more consistent and expected pattern than observed with the Census vacancy rate measure. Vacancy rates are much higher among the counties that have experienced population declines than among those that lost population. In particular, both the mean and the median of the duration-weighted vacancy rate among Census tracts for counties that experienced population decline are almost double those among counties that experienced population growth between 2000 and 2008 (10.1 versus 5.2 percent and 5.6 versus 3.1 percent). In

addition, the distribution of vacancy rates within the counties with population decline is much more dispersed, includes much larger extreme values and is flatter than the distributions within growing counties. This point is captured by differences in the standard deviations (12.4 versus 6.7 percent), differences in the 95th and 99th percentile values (33.5 versus 16.8 and 53.4 versus 30.5 percent) and differences in kurtosis or peakedness (23.5 versus 87.2). The only statistical measure at odds with this pattern is skewness, which measures the degree to which the distribution is tilted to the right of the average value toward larger values. I expected less skewness for the growing counties, but just the opposite was found.

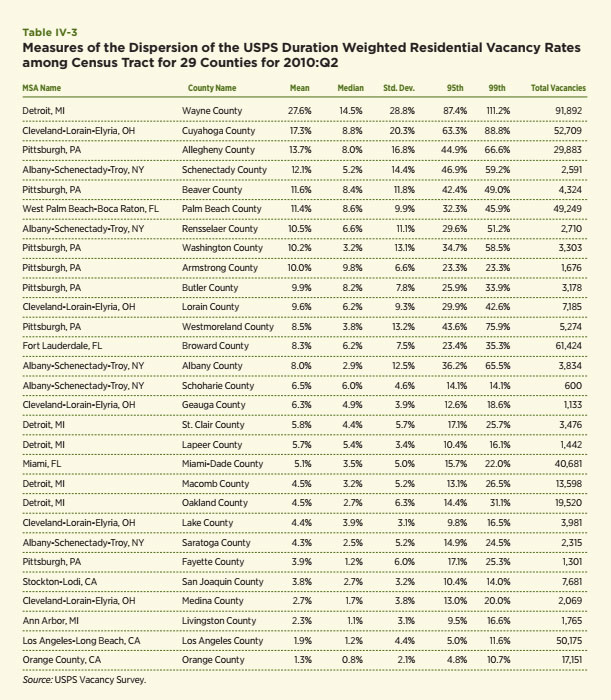

The same analysis is conducted at the Census-tract level for each of seven metro areas chosen for special attention in this study. Selected statistical measures are presented for each of the 29 counties within these metro areas (see Table IV-3). The counties are ranked by the mean average duration-weighted vacancy rate using 2010:Q2 data. The patterns in these results are striking and seem to offer strong confirmation of the central hypothesis of this section — declining cities have higher average vacancy rates and many more extreme values indicative of potential tipping points. This is most evident among the counties that encompass the central cities of the declining metro. For example, Wayne County, which includes the city of Detroit, has an average duration-weighted vacancy rate of 27.6 percent and five percent of its Census tracts have rates in excess of 87.4 percent. The 99th percentile value is an amazing 111.2 percent, a Census tract with a simple vacancy rate of 40 percent, but an average duration of residential vacancy that exceeded 1000 days, almost three years. The next three also fit the notion of a declining city or county — Cuyahoga, Allegheny and Schenectady. The duration- weighted vacancy rates exceed 12 percent and have standard deviations that are two to three times larger than their means. Two of the classic growing areas — Los Angeles and Orange County — are at the bottom of the list and the statistics confirm a much tighter and less dispersed vacancy pattern among them relative to any of the other areas by a large margin.

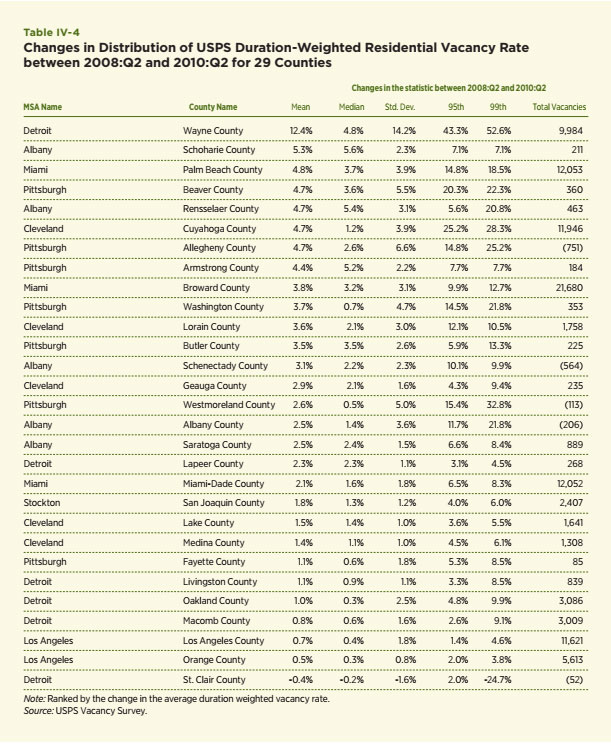

Another attribute of the USPS data is its ability to capture some of the changes occurring since the beginning of the Great Recession and the current crisis. This is done by comparing data in 2008:Q2 and 2010:Q2.26 Changes in the various vacancy rate measures are contained in Table IV-4 and again sorted by the largest to smallest changes in the duration-weighted vacancy rate.

The results strongly support the notion that markets in decline — including both the Rust Belt and the Sun Belt cities — can expect to experience increases in vacancy rates. All but one of the counties shows an increase in the duration-weighted vacancy rate during this two-year period. Wayne County also tops this list with an increase of 12.4 percent (15.2 to 27.6 percent). Note, too, that the standard deviation measures have increased in every county except St. Clair County, which is a suburban county in the larger Detroit metropolitan area. Similarly, the two measures of the extreme percentiles have increased for every county except St. Clair. Still, the Sun Belt has yet to experience anything like the vacancy rates in the declining cities.

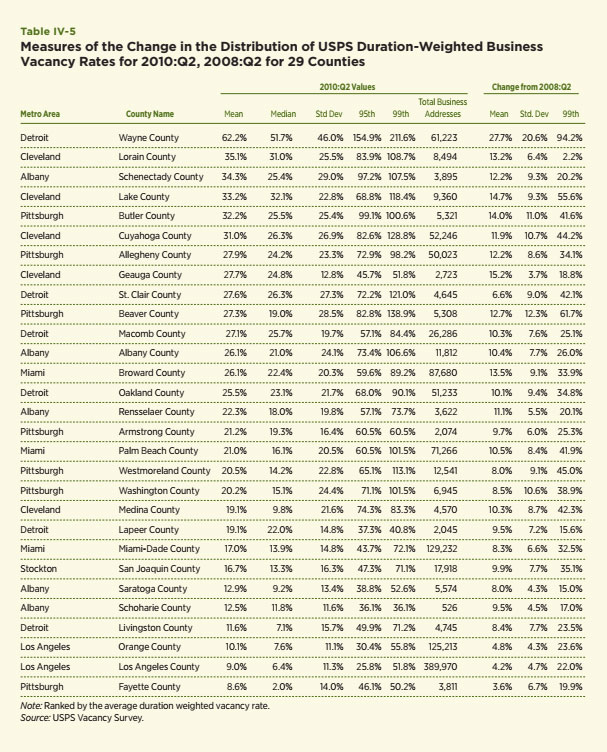

This paper, like most in the literature, focuses upon residential real estate owing to data availability. The USPS data offer an unusual opportunity to access and evaluate information about nonresidential property. It tracks the number of business addresses, the number of vacant business addresses and the duration of the vacancies. The same duration-weighted measure of business vacancies is computed using this information and provided in Table IV-5. The information includes 2010:Q2 data as well as changes since 2008:Q2 and are ranked by the 2010:Q2 business vacancy rate.