Over the past year, several semiconductor manufacturers announced plans for multibillion dollar investments to construct semiconductor manufacturing production facilities, or fabs, in the United States. In November 2021, Samsung announced a $17 billion investment in Taylor, Texas. Just two months later, Intel selected Licking County, Ohio as the site for two new fabs and an investment of $20 billion. More recently, Micron revealed plans in October 2022 for a $100 billion investment to build a megafab semiconductor manufacturing facility in Clay, New York over the next two decades. These investments and the jobs that come with them are considered a big win for local communities and the companies are heavily recruited by economic developers. This fierce fight for fabs is only heightening in intensity as a result of several geopolitical and economic developments.

Semiconductors are computer chips and they are an essential component in the production of phones, cars, medical devices, and multiple other electronic products. Demand for these chips has increased in recent years driven by growth in several markets including electric vehicles, telecommunications, and smart devices. At the same time, the semiconductor supply chain has been disrupted by COVID-19 shutdowns, natural disasters, and energy shortages. The result of these disruptions has been a significant global shortage. This shortage has highlighted the contribution of domestic semiconductor manufacturing to economic security and national defense and the striking decline of US and European dominance in the sector.

Demand for these chips has increased in recent years… At the same time, the semiconductor supply chain has been disrupted by COVID-19 shutdowns, natural disasters, and energy shortages. The result of these disruptions has been a significant global shortage.

In 1990, the US was home to 37 percent of global semiconductor manufacturing capacity, but this fell to 12 percent by 2020. Europe has seen a similar pattern with manufacturing capacity falling from 44 to 9 percent over the same period. Asian nations, by comparison, have increased their manufacturing capacity. While China, Taiwan, South Korea, and Japan accounted for 19 percent of capacity in 1990, their share grew to 73 percent by 2020. This shift has partially resulted from explicit national strategies to attract manufacturing and pursue leadership in the global semiconductor market. China, Taiwan, Singapore, and South Korea have offered manufacturers incentives and investments equivalent to at least 25 percent of the cost of ownership. The incentives in the US and Europe have been significantly lower at 10 to 15 percent.

In an effort to reverse this trend, Congress passed and President Biden signed the bipartisan CHIPS and Science Act in August 2022. The legislation was designed to improve the US’s global standing in the strategically important semiconductor industry. The CHIPS Act includes $39 billion in manufacturing incentives and a 25 percent investment tax credit for capital expenses for semiconductor manufacturing companies. The European Union is also considering the European Chips Act that is likely to be adopted in early 2023 and will aim to double the continent’s share of chip manufacturing from 10 to 20 percent.

With more incentives flowing from federal governments and a backlog of demand, the number of announcements related to billion dollar fab construction projects will likely grow. In this blog post, we explore the factors that are at play when companies select a location. We also look at why state and local policymakers aggressively court these facilities and what these announcements mean for the communities that will be home to these manufacturing facilities.

In 1990, the US was home to 37 percent of global semiconductor manufacturing capacity, but this fell to 12 percent by 2020.

Factors for Location

Resources for Production

There are a number of geographic features and resources that are critical when firms select a location for a manufacturing fab. First, seismic activity is extremely problematic for the manufacturing process. State of the art computer chips like those in your smart phone have 16 billion transistors (on/off switches used for processing), each only four nanometers wide (slightly larger than the diameter of DNA). Even the smallest vibrations can result in errors when manufacturing these transistors. Fabs cannot be located near areas of seismic activity such as places with a large number of earthquakes, big roads, or airports. Places where natural disasters such as tornados and hurricanes occur regularly can also have negative effects on the manufacturing process. Seismic activity or power disruptions caused by these events can bring production to a halt and result in millions of dollars in lost production.

Additionally, fabs require a lot of water. Estimates are upwards of 10 million gallons a day (the average person uses 50 gallons a day). Manufacturers have invested in infrastructure that allows for the purification and reclamation of water used in their facilities. Drought conditions in Arizona have forced Intel, who has a large manufacturing presence in the area, to adjust their manufacturing technology to reduce water usage by 40 percent. As firms select new locations, those with abundant and sustainable water resources will have an advantage.

Megafabs can use 100 megawatt hours of electricity every hour. The amount of electricity used by a fab could power 50,000 homes. Electricity can represent as much as 30 percent of the facilities’ operating costs in some locations. For a location to be considered, electricity must be reliable and affordable. Power outages can take a fab offline and result in millions in lost revenues. In recent years, the industry has moved towards a reduction in energy use and shift towards electricity from renewable sources. This transition is being driven by political and social pressures to lower carbon footprints and financial pressures to lower costs and stabilize expenditures on one of the more volatile inputs. This has led to some firms in the sector pledging to use renewable energy. TSMC announced a commitment to expand its usage of renewable energy in 2020, including 25 percent of power consumed in fabs and 100 percent in other facilities. In its announcement of the New York fab, Micron announced a goal of 100 percent of energy coming from renewable sources in the new facility. In an interview following the announcement, Senator Chuck Schumer (D-NY) said the proximity to the hydroelectric plant in Niagara Falls was a contributing factor in Micron’s selection of Clay, New York.

Fabs employ thousands of workers. There are two factors at play in recruiting workers for the manufacturing line. First, many of the production jobs do not require education beyond a high school degree, but workers do need significant on-the-job training that will prepare them to operate the manufacturing machinery. Companies often work with local higher education institutions and workforce development organizations to develop curriculums and apprenticeships that will prepare the local workforce for employment on the line. Regions need to have existing infrastructure that can provide a pipeline for workers.

The engineers and executives that run the fab will be recruited from a more global labor market. Companies need to consider if the location is somewhere that these people will want to live. High quality of life and access to amenities make it easier to attract professionals for these jobs.

Incentives

Economic incentives are also a factor in location decision-making. Traditionally, states and local governments offer packages of subsidies and incentives to attract these facilities to their communities. The largest portion of these come in the form of tax credits or abatements that allow the companies to save on property, sales, or employee income taxes. These incentives packages offer benefits over an extended time horizon (multiple decades) and are contingent on the firm meeting investment and/or employment targets. In addition, many localities pledge to develop local infrastructure, such as roads and utilities. Commitments to invest in the employee pipeline through the development workforce preparation programs and research spending at local colleges and universities are also common in incentive packages. With the passage of the CHIPS Act, the federal government is also offering incentives to semiconductor firms investing in advanced manufacturing facilities.

Recent Fab Announcements

SOURCE: Arizona, Texas, Ohio, New York.

Why Are Fabs So Sought After?

The primary reason that local communities hope to attract semiconductor manufacturing is that each facility can bring hundreds if not thousands of high-paying jobs. Many of these jobs can be filled by workers with a high school degree and on-the job-training. In this section, we look at the impact that these sectors can have on regional employment.

Overview of Semiconductor Employment

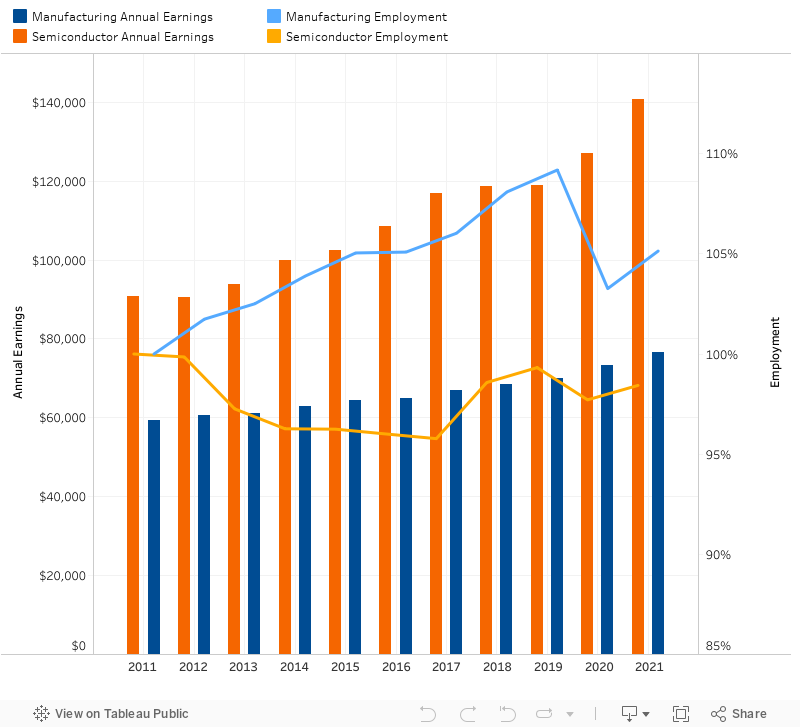

In 2021, the semiconductor manufacturing industry employed 393,000 workers in the US. Employment in the semiconductor manufacturing sector has been stable over the past 10 years. The manufacturing sector has grown steadily between 2011 and 2019, but even after a dip in 2020 from COVID-19 shutdowns, the larger manufacturing sector still experienced 5 percent growth over the same time period. As the announced fabs come on line, employment is expected to expand in the sector. There is a large pay differential between the semiconductor industry and the larger manufacturing sector. The average worker in the semiconductor sector earned $140,772 in 2021 vs $76,580 across the broader manufacturing sector.

Annual Earnings and Employment in the Semiconductor and Manufacturing Sectors, 2011-21

SOURCE: US Bureau of Labor Statistics, QCEW data for NAICS 33441 and 333242.

For this analysis, I define the semiconductor manufacturing sector as the combination of two industries. The first is Semiconductor and Other Electronic Component Manufacturing (NAICS 33441). This includes all firms that design and manufacture the computer chips that we integrate into our electronics such as phones, computers, and telecommunications devices. I have also included employment in the Semiconductor Machinery Manufacturing Industry (NAICS 333242). These firms manufacture the equipment that outfit the fabs to make the chips.

The two sectors are not equally distributed across the US. Ten states account for 71 percent of the industry’s employment. The largest segment of the industry is in California. California is the hub of the design segment of the industry and employs many of the engineers who develop the architecture for the chips that will eventually be manufactured elsewhere. As a result, the pay employed to these specialized engineers is nearly $100,000 more a year than the national average of $140,772. Texas is home to manufacturing facilities for Texas Instruments and Samsung. Both Oregon and Arizona host several Intel manufacturing lines. New York’s manufacturing is dominated by GlobalFoundries with facilities in East Fishkill and Malta, New York.

Semiconductor Employment by State

SOURCE: US Bureau of Labor Statistics, QCEW data for NAICS 33441 and 333242.

The table below provides details on the 20 most common occupations in the semiconductor manufacturing industry. These 20 occupations account for nearly two-thirds (64 percent) of all workers in the Semiconductor and Other Electronic Components Industry (NAICS 334400). The most common occupation is an electronic assembler. Other titles found on the manufacturing line include “semiconductor processing technician,” “inspectors, testers, sorters, and samplers,” and “miscellaneous assemblers and fabricators.” Companies with large manufacturing facilities often offer paid apprenticeships or training programs to individuals without experience in a fab.

The industry also hires a large number of bachelors and graduate degree holders with specialties in industrial engineering, computer hardware engineering, electrical, and mechanical engineering. In general, workers with a high school diploma earn $35,000-$60,000/year depending on the position. Engineers working in the industry receive average annual pay ranging from $100,000 to $135,000 with managers making more.

Most Common Occupations in the Semiconductor Industry

SOURCE: US Bureau of Labor Statistics, Occupational Employment and Wage Statistics for NAICS 334400.

Impacts in Other Sectors

When a fab is built in a region, the employment impacts reach beyond the jobs created at the facility. The details of the Micron announcement projected 9,000 jobs with Micron at the facility but an additional 41,000 jobs across the state. A number of sectors will receive these direct benefits.

Construction Phase

Facilities of this scale require years of construction before production can begin. The Micron project in New York laid out plans for $100 billion in investment over the next 20 years. Site preparation for the first $20 billion phase will begin in 2023 and construction will occur throughout 2024. When Intel announced a $20 billion project earlier this year, they estimated it would support 7,000 construction jobs over the course of the construction. Communities can expect to see large demand for construction professionals and building materials in the region as the site is cleared, the foundation is poured, the building is erected, and advanced HVAC systems are installed.

Operations Phase

When fabs locate in a region, a number of suppliers follow to help support the local manufacturing ecosystem. The firms that make the equipment used in the fab set up local offices to support the operations. The Micron announcement was followed by a commitment from Edwards Vacuum, an equipment supplier, to build a $319 million manufacturing facility in Genesee County. Local businesses offer IT support, legal and business services, and security for the facility. Local utilities provide critical inputs. Demand for transportation, warehousing, and storage in the region increases. Hotels offer visitors a place to stay on work travel. Local colleges and universities can offer curriculum, training, internships, and research collaborations that can serve as a pipeline for workers and innovation.

In addition to impacts on the supply chain, the creation of high-paying jobs in the region increases demand for goods and services among the local population. This creates demand for restaurants, retail establishments, health care, childcare, and real estate.

A Caveat

When reviewing these announcements, it is also important to note that they are subject to change. Many of these multibillion dollar announcements related to advanced manufacturing promise significant investments over a decade or even longer. Over the course of the extended timelines for these megaprojects, technology will evolve and market forces will shift. Reports in recent weeks have warned of a potential downturn in the sector in coming months. The sector’s volatility means that some of these announced projects will never reach expected capacity. One recent example is the Foxconn display manufacturing plant in Wisconsin. The project was originally announced in summer of 2017 as a $10 billion investment. The plan was scaled down to $672 million in spring 2021. The state also reduced the tax credits offered for the project from $2.9 billion to $80 million. Not all changes will be as severe as those seen in Wisconsin, but it is important to remember that projections made at the time of announcement may differ from what occurs after construction is complete and these fabs open their production lines.

Conclusion

Given the US’s significant investment in semiconductor manufacturing enabled by the CHIPS Act, we will likely see a number of new announcements in coming years. States and local governments will actively compete through grants, tax incentives, and subsidies to attract these facilities. These incentives are offered in hopes of attracting major employers who bring with them well-paid opportunities for skilled workers of all backgrounds. While these economic packages are important factors, regions must also meet the resource and workforce needs of these megaprojects.

ABOUT THE AUTHOR

Laura Schultz is executive director of research at the Rockefeller Institute of Government