It’s poised to be a big year for marijuana in New York State. Shortly after licenses were awarded by the Office of Cannabis Management (OCM), the first adult-use dispensary in the state opened on December 29, 2022, in New York City, with additional retail following both downstate and upstate within weeks. As the retail market expands, the team at the Institute is keeping their eye on a number of developments. Here are five of the trends that we will be watching.

-

Supply and Demand

One of the initial complexities of rolling out a legal marijuana market is uncertainty related to supply and demand. In general, states do not have good data about the number of existing marijuana users and their product preferences, nor do they know the number of new customers that may participate in the market now that marijuana is legal. This, in turn, makes it difficult to predict the number of dispensaries and the amount of crops to be grown and harvested that the customer base would support. These calculations are further complicated by the federal prohibition on marijuana which prevents the importing or exporting of product; legal adult-use marijuana must be grown and sold only within the confines of the state.

If state officials get these estimates wrong, it could result in an inadequate supply of merchandise. Several states experienced shortages or near shortages in the early phases of adult-use legalization. Colorado (2014), Washington (2014), and Illinois (2020) all experienced low inventory concerns. Nevada (2017) declared a statement of emergency after one week of sales to permit officials to enact emergency regulations to help increase supply. States can also overestimate demand though, which can result in an unexpected surplus—both California and Oregon have struggled with a glut of merchandise—and drive down prices.

Another factor that impacts demand in the legal adult-use marijuana market is the proliferation of the illicit market. Legalization may entice some people who were curious about marijuana but refrained due to its illegality to become new consumers with the promise of a regulated, tested, and legal product. However, most customers will likely be those that either previously purchased marijuana products from a nearby state or from the well-established illicit market. The success of the legal state market will depend on how effective it is at encouraging users to abandon the illicit market and retain them as regular customers.

States have had varying success with cutting into the illicit market and no state has eradicated it completely. Depending on the taxes levied by the state, legal marijuana may be more expensive than comparable products in the illicit market. States including Massachusetts, Illinois, Oregon, and Michigan have all seen their state’s illicit market continue despite legalization. California has potentially struggled the most, with illegal sales reportedly outnumbering legal sales two to one. New York has a vibrant illicit market—the New York City Police Department (NYPD) estimates that there are 1,300 unlicensed marijuana stores in New York City alone—which will pose a challenge to regulators and law enforcement. Failure to rein in the illicit market will cut into legal sales and diminish the tax revenue for the state and localities.

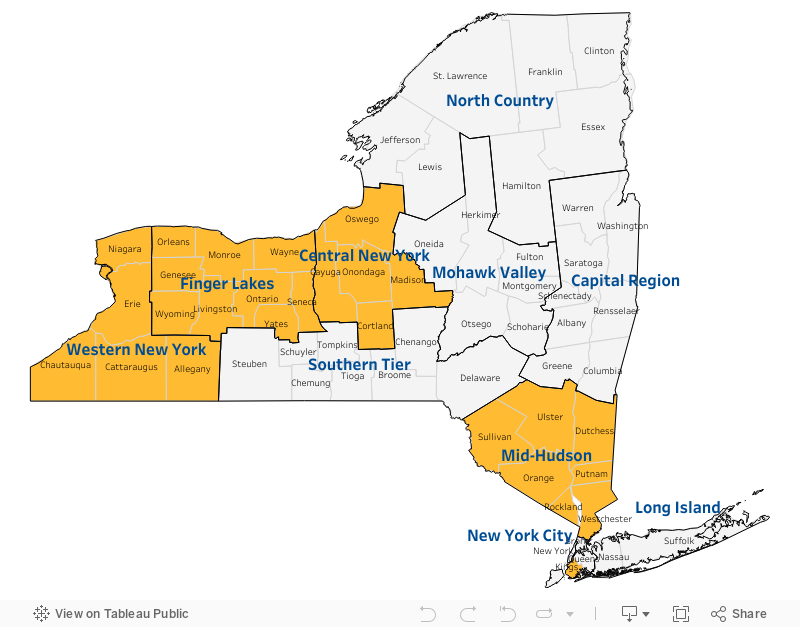

New York uniquely had a last-minute wrench thrown into their rollout plan which may have additional repercussions for supply and demand. A challenge to the state’s requirement that licenses would be available only to candidates that were impacted by the drug laws in New York resulted in an injunction to dispensary licenses being granted in five regions of the state: Brooklyn, Central New York, Finger Lakes, Mid-Hudson, and Western New York. That has effectively shrunk the size of New York’s market while the injunction is in place and may deflate demand from original projections. Cultivators in the impacted regions may now have to find other markets for their product. Depending on the outcome of the legal challenge, the ability of New York’s legal market to fully mature and operate may be delayed.

Regions Where Injunction to Grant Dispensary Licenses is in Place

■ = injunction in place

-

Marijuana Deserts

New York, like most of the states that have legalized adult-use marijuana, allowed local governments to opt out of allowing marijuana dispensaries and/or consumption lounges in their jurisdiction. Cities, towns, and villages had until December 31, 2021, to pass a local law prohibiting dispensaries and/or consumption sites. Once that deadline passed, localities that took no action were automatically entered into the marijuana market. In keeping with trends in other states, many localities exercised that prohibition option; according to the Institute’s Marijuana Opt-Out Tracker, approximately 50 percent of municipalities have opted out of permitting dispensaries and 58 percent have chosen to prohibit consumption sites. This has resulted in some “marijuana deserts” in the state where no or few dispensaries will be able to operate. In Putnam County, for example, only one municipality currently has allowed dispensaries. Nassau and Suffolk Counties—with a combined population of approximately 2.8 million people—only had sixteen municipalities opt in. While delivery will be available in New York State (more on that below) the result of these opt-outs is that many residents will not live in proximity of a dispensary which may also impact sales and revenue, especially if those consumers are already used to buying from the illicit market.

However, the decision to opt out is not permanent, so one issue to watch in 2023 is how many municipalities may reverse their decision and lift their prohibition. The Institute’s research found that many municipalities originally opted out “for now” and were open to reversing the decision after seeing how legal sales played out in other municipalities or with additional guidance from OCM on rules and regulation. Since the December 2021 deadline, a handful of municipalities have already rescinded their opt-out, even prior to the first dispensary opening in the state. As the legal sale rollout continues, will the lure of tax revenues be enough to compel some other municipalities to reconsider?

Additionally, as previously mentioned, a legal challenge to licensing requirements means that regardless of opt-out decisions, dispensaries cannot be opened in five regions of the state. Until the injunction is lifted, residents of those areas will be without options for local legal purchase.

-

Regional Dynamics

One of the justifications for early adoption of a retail cannabis market is that a state could generate tax revenue from consumers in other states crossing the border to purchase legal cannabis.[i] At this point, much of the Northeast US has established a legal retail cannabis market. Massachusetts was the first state on the east coast to open retail dispensaries in November 2018. The Bay State was followed by Maine (October 2020). Over the past year, dispensaries have opened in New Jersey (April 2022), Vermont (October 2022), and Connecticut (January 2023). In just over four years, the first mover advantage that made Massachusetts a destination for cannabis purchases evaporated as all but one of its neighboring states also created retail markets.

A trend to watch is what happens to sales in Massachusetts as the dispensary infrastructure in New York and Connecticut is built up. The news broke in December that the state will be seeing its first closure as a dispensary in Northhampton shuttered. It is still too soon to tell if the closure is just a unique event, a signal of broader economic and market trends, or the result of evaporating out-of-state demand. Over the coming months, it will be interesting to track Massachusetts cannabis sales data, in particular from dispensaries located near the borders to see if there are downward trends.

As cross-state purchases may decline along the coast, New York still shares a long border with a state that has yet to legalize retail sales. Will dispensaries closest to Pennsylvania outperform businesses that serve a more local New York population? And, will we see cars with Pennsylvania and Ohio license plates in Fredonia, Jamestown, Elmira, and Binghamton dispensary parking lots?

-

Delivery

When the Marihuana Regulation & Taxation Act (MRTA) was passed in New York in 2021, the legislation provided for the licensing of marijuana delivery services. Marijuana delivery is a relatively new phenomenon—Oregon was the first state to permit it in 2017—and it has not yet become universal in states that legalize adult-use marijuana. While adult-use marijuana delivery is currently approved in California, Colorado, Connecticut, Massachusetts, Maine, Michigan. Nevada, Oregon, New Jersey, and New Mexico, it is not permitted in Alaska, Arizona, Illinois, Montana, Rhode Island, Vermont, or Washington. Even within the states where adult-use delivery is allowed, there is no uniformity in regulation. States have different limits on who can deliver (dispensaries only vs. a delivery service) and where deliveries can be made (both geographic location and type of building). For example, in Oregon, delivery was originally only available to customers in the same jurisdiction that the marijuana retailer was located. Now, municipalities in the state can opt-in to allow deliveries from adjacent jurisdictions. Colorado similarly requires municipalities to opt-in for delivery, though many states have no such requirement. Most, but not all, states prohibit delivery to hotels (California being the exception to the rule). Because a “one-size-fits-all” approach to marijuana delivery in the states has not yet evolved, there is still room for innovation and experimentation with these types of policies.

The delivery guidance issued by the New York State Office of Cannabis Management does not put any limitations on geographic regions of the state where delivery can occur, so an issue to watch is what business models delivery licensees will adopt as the legal market continues to roll out in the state. While some delivery services may opt to set a more limited delivery radius, others may decide to venture into the marijuana deserts referenced above to deliver to underserved customers. Given the uncertainty on when the court injunction will be lifted in Brooklyn, Central New York, Finger Lakes, Mid-Hudson, and Western New York, however, it is unclear if delivery companies will be willing to invest in serving these communities given that the prohibition on dispensaries may be short-lived. It also remains to be seen how much of the sales market in New York will be from delivery. More broadly, there is the question of whether people that became accustomed to the ease of having items delivered during the pandemic will prefer going to a brick-and-mortar dispensary to peruse the merchandise in person and engage with budtenders on what strain and potency of marijuana would be best suited for them.

-

Data Development

Researchers and market watchers are eager to track the early days of the emerging retail cannabis sector in New York. Data on licenses, employment, sales, and tax revenue can be a valuable resource for understanding supply and demand across the state, the fiscal impacts for the state and local communities, and business development. Every state has taken a slightly different approach to how it reports data related to cannabis.

New York’s Office of Cannabis Management released its first annual report in 2022. That report included information on several topics: breakdowns of revenues generated through the medical cannabis, cannabinoid hemp, and adult-use cannabis markets, as well as data on the money generated through application and renewal fees, fines, and tax revenue. The report also included information on Registered Organizations manufacturing and dispensing cannabis, professions of Registered Practitioners participating in the medical cannabis program, permitting and licensing activity in the Cannabinoid Hemp program, and the number of applications for Adult-Use Cannabis licenses. Data from State Fiscal Year 2022 (April 1, 2021 to March 31, 2022) and the first half of State Fiscal Year 2023 were in the report.

The New York State Department of Taxation and Finance further provides monthly data on state revenues generated through Excise and User Taxes and Fees generated through the Medical Marijuana and Adult-use Cannabis programs. While the publication of this data is more frequent, the data itself is less detailed. It includes total amount collected, but does not provide a breakdown of revenue by fees, potency tax, or sales tax. An additional limitation of the data published is that it is statewide and does not currently allow for tracking of trends at a more local level.

As states roll out adult-use cannabis programs they often iterate on data reporting practices. New Jersey’s Cannabis Regulatory Commission has released three reports to date. The first included weekly data on sales and the number of transactions (in the first five weeks, the average sale was for $99.80). Subsequent reports have been less granular and instead provide information on total recreational and medicinal sales on a quarterly rather than weekly basis.

As the most mature market in the region, the Massachusetts Cannabis Control Commission has a more sophisticated data reporting system. Their website includes an online dashboard that presents weekly and monthly sales data, breakdown of sales by product category, average retail price, cultivation activity, current status of licensing activity, and demographic data on marijuana establishments. In addition raw data is provided on the location and ownership of marijuana establishments and daily sales by category. The abundance of information published allows for a close monitoring of the market by interested parties.

Once up and running, New York is poised to be the second largest market in the country. The data the state collects could be an invaluable resource for researchers and policymakers seeking to understand how the market has developed and make visible emerging trends. This is an excellent opportunity for the state to take a thoughtful approach to data collection and transparency.

The coming months may reveal answers for many of these questions. Check back with the Institute’s In the Weeds series to continue to track the evolution of adult-use cannabis policies and their impacts.

ABOUT THE AUTHORS

Heather Trela is director of operations and fellow at the Rockefeller Institute of Government

Laura Schultz is executive director of research at the Rockefeller Institute of Government

[i] A reminder to the owners of the cars with NY plates in the western MA dispensaries: transporting cannabis across state lines is still a federal offense even if possession is legal in both the origin and destination states.