There has not been a new city incorporated in New York State since 1942 despite multiple attempts by more than a dozen communities to win state approval for city status. The Village of Hempstead in Nassau County has recently announced that it is once again exploring the option of cityhood. At the urging of the mayor, the Village Board appointed a 10-person commission, a City Charter Commission Advisory Board, to study the pros and cons of reincorporation and to draft a proposed city charter to submit for state approval. As the state’s largest village, Hempstead is well situated to highlight the outdated and ossified municipal structures to which state and federal assistance programs remain keyed. And the history of municipalities attempting to incorporate demonstrates that winning approval for a new city incorporation from Albany remains a nearly impossible political quest for a few reasons. This first piece in a two-part exploration considers the motivations for Hempstead’s cityhood movement and the fiscal incentives behind and challenges ahead of that effort. (Read “Part Two: The Process and Politics of City Incorporation” here).

The Case for City Status for Hempstead

The motivation behind the effort to incorporate the village of Hempstead as a city is twofold. The first impetus can be described as civic prestige. Although New York does not legally classify its municipal forms based on population size, there is an unspoken narrative of progress in municipal development wherein higher population density, longevity, or economic growth are popularly associated with the city form of government.1 That is, there is a popular misperception that villages become cities upon reaching a certain population threshold. While 98 percent of New York’s 61 cities outside of New York City were initially incorporated as villages, state law does not require that villages transition to cities after reaching a certain size, or that cities revert to a village if their population declines.2 As such, in New York, some villages (including Hempstead) are larger than many cities.

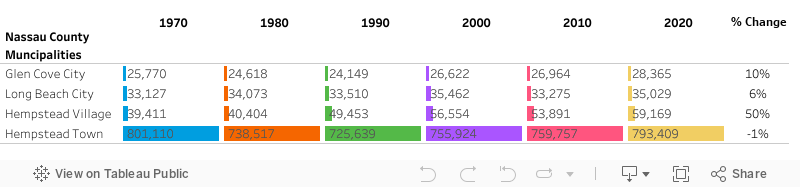

Settled by the Dutch in 1664, the village of Hempstead is one of the state’s oldest communities. Its growth as a center of commerce and trade coincided with its incorporation as a village in 1853. Presently, the village of Hempstead comprises just 7.5 percent of the town of Hempstead’s sizeable population, of which it is a part, but its centrality as a commercial “hub” along with its size (59,169—the largest village in New York State) all stand as arguments for converting this village to city status.3 The village of Hempstead is also larger (in terms of population) and has grown more significantly than either of the two existing cities in Nassau County—the cities of Glen Cove and Long Beach.4 (See chart below.)

Relative Population and Growth of the Village of Hempstead to Other Nassau County Municipalities

SOURCE: “Population Data, Resources, and Publications,” New York State Office of the State Comptroller.

If the village of Hempstead were to become a city, it would be the 11th largest in New York State and well above the average (37,391) and median (19,800) size of New York cities (excluding New York City but including the other “big five” cities denoted in gray-shading in the table below). Thus, for many city supporters, Hempstead’s longevity and population warrant its transition to city status as better reflecting its urban character and diversity, and to allow a community of its size to claim a fairer share of state assistance.

Populations of New York’s Cities (excluding NYC)

The second motivation is financial: cities receive substantially more state aid than do town and village governments. In short, state funding formulas favor cities based on the assumption that they require more aid given the complexity and problems that are commonly associated with urbanized areas, including higher population density, more diverse demographics, higher concentrations of poverty and crime, aging infrastructure, etc. However, in New York State, city status is not restricted to communities of a particular size and there are no territorial or population requirements for incorporation as a city. Thus, the funding formulas have been criticized as particularly disadvantageous to larger villages which have many of the same challenges as mid-sized to large cities. The disparate funding formulas that are based on municipal class rather than municipal characteristics results in cities receiving the bulk of state funding. City status would therefore mean increased revenue for the village of Hempstead through the enhanced state and federal assistance given to city governments.

If we compare the village of Hempstead to Nassau County’s two incorporated cities, the cities of Glen Cove and Long Beach, it is evident that, although Hempstead is larger and has exhibited greater population growth, it receives less per capita aid through the Aid and Incentives to Municipalities (AIM) program—New York’s primary program for sharing general revenue with its localities. The figure below summarizes annual AIM funding for the different municipal classes in 2022. Without the big five cities included (Albany, Buffalo, Rochester, Syracuse, and Yonkers), the total AIM funding for cities falls from $647,093,629 to $204,992,046. AIM funding for all municipal classes (cities, towns, and villages) has remained basically flat since 2009.

Annual AIM Funding for Municipal Classes, 2022

This difference in funding formulas means that the Village of Hempstead receives $2.8 million less than the City of Glen Cove and $3.3 million less than the City of Long Beach, despite its larger population. That translates to a $79-$89 difference in AIM received per capita.

Differences in AIM Funding, 2021

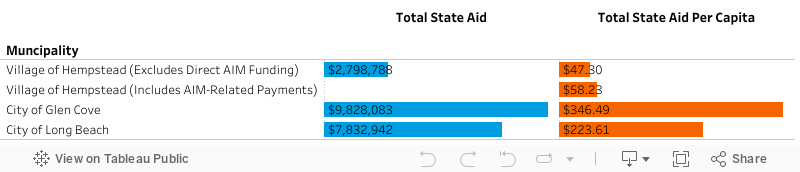

Factoring in other forms of state aid (restricted as well as unrestricted), reveals similar discrepancies. In the figure below, the total direct state aid received across 14 categories of state assistance is included. In 2019, the executive budget eliminated direct AIM payments and replaced it with AIM-related payments funded through the counties’ share of state sales tax revenues for villages and towns where AIM constituted less than 2 percent of the municipal budget. Hempstead was one such village—thus its 2021 state assistance did not include direct AIM payments from the state, although it received the same funding level ($646,743) via Nassau County’s share of state sales tax revenue. With AIM-related payments included, the per capita assistance for the village of Hempstead is $58.20 (still far below that received by Nassau’s two cities).5

Total State Aid Received, 2021

SOURCE: "Local Government Data Search," Open Book New York, New York State Office of the State Comptroller.

An exploration of the subcategories of state assistance (see chart below), shows that Nassau County’s two cities received state assistance not received by the Village of Hempstead in the categories of general government, transportation, and direct-AIM. Conversely, the Village of Hempstead received greater state funding than did either Glen Cove or Long Beach in the category of public safety.

Categories of State Aid and Funding Received in 2021

Reincorporating as a city would also allow Hempstead to claim a greater share of the county sales tax revenue.6 Nassau county has a minimum combined county tax rate of 8.625 percent. The state retains 4.0 percent, while 4.25 percent is retained by the county, and .375 percent goes to the Metropolitan Transportation Authority (MTA). The county shares .75 percent of its total with municipalities, with one-third (.25 percent) of that allocated to Nassau’s three towns and two cities (based on population). Villages receive an amount not to exceed one-sixth of the remaining (after towns and cities receive funding).7

A review of the 2019 and 2021 budgets of the three municipalities reveals that the cities of Glen Cove and Long Beach received substantially greater assistance from the distribution of Nassau County sales tax revenues (see table below). The Village of Hempstead received $1 million less than Glen Cove and more than $2.6 million less than the City of Long Beach in sales tax distribution.

Nassau County Sales Tax Distribution

There are certain taxes that cities can levy that villages may not, including a consumer utility tax (an amount of approximately $460,000 for the City of Glen Cove in 2021). City status would thus give the village of Hempstead greater diversification of its tax base. Note also that in 2021 the Village of Hempstead received $1.2 million less in mortgage recording tax share than did the cities of Glen Cove and Long Beach. Becoming a city would increase Hempstead’s share of the state mortgage recording tax. Whereas cities receive the full distribution of taxes collected on mortgages within their jurisdiction (less county administrative costs), villages only receive a fraction of the town’s share, calculated as a proportion of its assessed value to that of twice the town’s.8 Similarly, funding for New York’s Consolidated Local Street and Highway Improvement Program (CHIPS) differs by municipal class: “42.7% for cities, 18.5% for counties, 28.1% for towns, and just 10.7% for villages). Amounts so allocated to each municipality class are then apportioned within that class based on the relative number of lane miles, exclusive of parking lanes, under the maintenance jurisdiction of each municipality.” Additionally, city status allows villages to transition the bulk of the cost for maintaining a court system to New York State. Per the FYE 2023 Village of Hempstead budget, the village justice court budget is funded at $646,804.

The story of federal assistance is similar: city incorporation would increase the amount of federal assistance received by the village of Hempstead, again, because cities, as a class, receive enhanced funding based on the presumption of more complex service needs. One can see these differences at work in Nassau County: the cities of Glen Cove and Long Beach currently receive more federal funding in total and per capita than the village of Hempstead, again despite their smaller populations. The village of Hempstead currently receives only $6.12 in per capita federal assistance compared to the $220 and $375 per capita received by the cities of Glen Cove and Long Beach, respectively. (See Figure 8.)

Categories of Federal Aid and Funding Received in 2021

New York’s property tax cap, made permanent in 2019, limits municipalities to increases in the annual tax levy to no more than two percent or the rate of inflation, whichever is less. While Hempstead has not overridden the property tax cap for the past several years, the village has exhausted over 75 percent of its constitutional tax limit —a “red-line” indicator that the Office of the State Comptroller associates with limited fiscal capacity and reduced budgetary flexibility. Because the village is pushing up against its constitutional tax limit, it becomes less able to rely on real property tax increases moving forward. (See Figure 9.) Becoming a city would not alter Hempstead’s constitutional tax or debt limitations, but it would provide additional new revenues sources and would allow greater flexibility in determining the governance structure as cities can choose mayor-council, council-manager, or a commission organization of city government.9

Village of Hempstead Percent of Constitutional Tax Limit Exhausted, 2008–20

The Case against City Status

The village of Hempstead’s quest to become a city runs counter to state municipal trends. As illustrated below, the peak of new city incorporations in New York in the 1890-1910 period coincided with urban growth. Prior to the revision of village powers under the General Village Law of 1927 and the extension of home rule powers to larger villages, several villages reincorporated as cities to claim greater local powers and authority. But since village powers have subsequently grown and become less distinguishable from those wielded by cities, the arguments in favor of converting villages to cities began to dissipate. Post-1950s deindustrialization and slowed growth in cities further dampened the demand for new city formations. After a Suburban Town Law and classification was introduced in 1962, giving large or metro-adjacent towns enhanced powers, the argument that a city government is necessary to provide general services to large population centers eroded.

New City Incorporations in New York State

Population Change by Class, 1910–2020

As the growth shifted to towns and suburbs, however, some communities in metro-adjacent areas sought greater control over zoning to forestall the increased housing density associated with growing development. Thus, the creation of new villages and proposed cities was sometimes motivated by a desire to secede from the town so as to secure more localized decision-making control over zoning and development. In the 1960s, for example, several villages in Rockland (including Haverstraw, Suffern, Sloatsburg, and Spring Valley) and Westchester Counties (including the villages of Mamaroneck and Harrison) pursued city status, as a response to the influx of residents from New York City. Repeated, failed efforts to reincorporate the village of Kenmore—a first ring suburb to the city of Buffalo in Erie County between 1930 and 1970, similarly reflected suburban anxieties over urban encroachment and development. Moreover, as the politics of urban areas trend differently than those in the surrounding suburbs, the creation of new municipalities allowed residents in those communities to choose dedicated representation as a jurisdiction separate from the surrounding town. Cityhood efforts have thus become increasingly contentious as synonymous with secession by wealthier, white enclaves in otherwise unincorporated areas of the town or county.

In Hempstead’s case, the village is much more diverse than the surrounding town. Only 13.4 percent of the village’s population are non-minority (White) versus 61 percent of the surrounding town. Race and class are therefore likely to play a role in the relative level of community support for making Hempstead a city. City status for this minority-majority community would arguably enhance self-governance and prestige, asserting its independence from the larger, less diverse town. On the other hand, reincorporation as a city would likely eliminate the sole Democratic-held seat on the town board currently elected by the village of Hempstead residents. Moreover, many of Hempstead’s voters, including its minority residents, have a preference for the village form of government as smaller, more efficient, and idyllic, and express a wariness of the perceived negative connotations often associated with cities. Particularly in Westchester, Nassau, and Suffolk counties, village governments were created and favored for perceived quality of life benefits, including lower housing density, neighborliness, and exclusivity. Residents, in other words, may be psychologically attached to the village as a municipal form, believing village-style government better reinforces certain smaller, more intimate community characteristics and governance.

Most importantly, there are both costs and limitations to city status that will offset the revenue gains of enhanced state and federal aid. While becoming a city would relieve village residents from paying town taxes in the future, it would not eliminate their responsibility for any prior town indebtedness.10 If reincorporated as a city, the charter would need to account for the transfer of village property, contracts, obligations, and liabilities. Similarly, the charter would have to provide for the legal dissolution of the former village upon the election of city officers. The continuation of any services formerly provided by the town would have to be assumed by the new city government funded by taxes previously paid to the town, or else by new city taxes, under equalization rates which may differ from the former village.11

In terms of additional obligations, cities typically bear responsibility for the administration of elections and civil service law, and for the maintenance of county and state highways within the city limits. While becoming a city would transfer administration of a village’s court system to the state (something that could also be accomplished by the dissolution of the village court with the transfer of the service to the embracing town), state law requires cities to provide municipal fire services, assessment, and tax collection services. Again, specifications of such would need to be addressed in the proposed charter and thus require study and consideration in the drafting process. The village of Hempstead funds a municipal fire department, tax assessment, and tax collection services as part of their current budget. Nonetheless, careful review will be required to determine what offsets would adhere to city status.

Most significantly, under Education Law 2(16)(b) and (c), when a new city is formed, any school district coterminous with that city, or which contains all, or a portion of the city, and a majority of the population of children, becomes by definition a city school district. Not only does indebtedness of that school district transfer to the new municipality, but city school districts are subject to more stringent constitutional tax limitations than are non-city-school districts (5 percent as opposed to 10 percent of the limit). Cities are also responsible for compensating school districts for uncollected property taxes—an obligation that is not imposed on villages. As such, the charter commission will need to carefully review the ramifications of city status given the differential obligations of maintaining a city-school district.12

Moreover, city residents would be ineligible from receiving exclusive services provided to residents, including senior services and free access to town parks and beaches. Part of the study process will entail a line-by-line analysis of the budget, with an eye for determining what current services provided by the town would offset the gains in state and federal assistance, and how the village would fare under the differential treatment of cities and villages in an array of state laws and regulations.13

Next Steps for Hempstead

The village of Hempstead’s newly appointed City Charter Advisory Board, comprised of village trustees and citizens, is likely to take a year or more to complete its study and draft a proposed city charter. Given the factors discussed above, they may ultimately be able to show that city incorporation would be financially advantageous to the community. Convincing village residents and local representatives to support the transition to a city status, however, is only part of the challenge. As will be discussed in Part II of this series, to succeed will require broader consensus and coalition building outside of the village to support the state legislation necessary for the approval of incorporation.

ABOUT THE AUTHOR

Lisa Parshall is a fellow at the Rockefeller Institute of Government and a professor of political science at Daemen University

[1] In New York, municipal classifications are not based on population size. Counties and towns are involuntary incorporations created by the state. Cities and villages are voluntary incorporations—that is, they may be incorporated out of town territory that is not already part of an incorporated city or village in response to local demand. Villages can be incorporated by local action under general law provisions subject to minimal territorial and populations requirements. New York banned the incorporation of villages by special law in 1874, although a dozen villages continue to operate under special charter. Under the General Village Law, the incorporation of a village involves a petition process followed by a public referendum approving the incorporation and the filing of a certificate of incorporation with the secretary of state. Upon incorporation, villages (and their residents) remain part of the town (or towns) in which they are located. Cities, on the other hand, must be created by a special act of the state legislature, although there is no minimal territorial or population requirements. As such, there are some cities that are smaller than villages, or are less populated than the surrounding towns. Cities are independent municipalities separate from the surrounding town (or towns). For more, see “Outdated Municipal Structures.”

[2] New York City, Albany, Hudson, Schenectady, Port Jervis, and Lackawanna were incorporated as cities; the remaining cities began their existence as incorporated villages. The city of Sherrill is a special case—though incorporated as a city, its charter specifies that it be governed as a village.

[3] The town of Hempstead’s population is 793,409 according to 2020 Census, making it the largest in New York State and one of the largest towns (or townships) in the United States. There have been suggestions to incorporate the entire town as a city, which would be the state’s second largest after New York City. As with villages, there are no population or territorial requirements for towns (indeed towns were often platted as subdivisions of the county prior to their incorporation and settlement). Many towns retain a more rural character, while others have substantial populations consequent to suburbanization and growth. New York’s smallest town in terms of population is the town of Red House in Chautauqua County with a population of 27 per the 2020 Census.

[4] In territory, the village of Hempstead (3.7 square miles) is smaller than Glen Cove (6.7 square miles) but larger than Long Beach (2.2 square miles).

[5] Direct AIM was restored for all towns and villages in the FYE2023 state budget but remained flat at its pre-2019 funding levels.

[6] Cities may enact their own sales tax (and 18 of New York’s cities currently do so) typically by preempting half of the county sales tax (up to 1.5 percent) although the combined county and city tax rate cannot exceed 3 percent. Tax Law §1262(d), provides that cities and towns receive a share of certain sales taxes related to hotel occupancy, restaurants, and other retail establishments. This law gives cities a choice to receive their share of sales tax revenues directly or as a credit toward property taxes levied by the county. Towns may only receive the revenues as a credit toward their county property tax levy.

[7] In 2018, 28 villages filed an Article 78 motion against Nassau County and several townships, including Hempstead, for failure to share the one-sixth share of the sales tax revenues from the three-quarters percent sales tax authorized by state tax law for distribution to municipalities. A Nassau County Supreme Court ruled in favor of the county and town, concluding that the amount is not automatic but is negotiable up to one-sixth. See “Judge Rules For County In Sales Tax Dispute.”

[8] Nassau County administrative code § 5-1.2 provides that where a town contains an incorporated village, the village be apportioned so much of the town’s portion “as the assessed value of said village, or portion thereof, bears to twice the total assessed valuation of the town.” In 2021, the proportion of the village’s full assessed value to that of twice the towns was .3 percent, or 3:1000.

[9] Constitutional debt and tax limitations of villages and cities are similar: Article VIII, § 4 of the New York State Constitution provides that no county, city, town, or village shall contract indebtedness which, including existing indebtedness, exceeds 7 percent of the five-year average full valuation of taxable real estate therein. There is an exception for cities having 125,000 inhabitants or more (except New York City), raising the calculation to no more than 9 percent. The New York State Constitution limits the taxing power of both cities and villages to 2 percent of the five-year average full valuation. The constitutional tax limit (which limits the overall amount of property taxes that can be levied) is different from the property tax cap (which limits the year-to-year increase in the tax levy).

[10] Town indebtedness is typically calculated as a ratio of the value of taxable property in the newly incorporated city to the total taxable townwide valuation as determined by assessment rolls the year prior to incorporation. Any such legacy costs, indebtedness, or continued obligations to the town would need to be addressed in the proposed charter.

[11] Many independent taxing entities (including school and special districts) have overlapping jurisdiction. Because municipalities do not all assess at full value (some assess above and some below full market value), equalization rates are applied to apportion tax responsibility to the municipal units (or segments of such units) that lie within each taxing jurisdiction. Equalization rates are calculated by dividing the total assessed value of a municipality by the total market value of the municipality.

[12] One significant barrier on new city incorporations was the constitutional tax limitation imposed upon city school districts. Article VIII, Sections 4 and 10 of the New York State Constitution restricted indebtedness for cities over 125,000, including public school taxes, to two percent of the annual average full valuation of taxable real property when population exceed 125,000. Thus, for example, when the village of Kenmore explored city incorporation in the 1960s, they were mindful that a population increase would impact the feasibility and savings of city incorporation. This constitutional tax limit for city school districts was repealed for small cities (under 125,000) in 1985. School districts are now subject to the Property Tax Cap that limits the annual growth in property taxes levied by school districts and local governments to two percent or inflation, whichever is less. The cap does not apply in New York City and a few large school districts. The Property Tax Cap can be overridden by sixty percent of voters (for school districts) or sixty percent of the total voting power of the governing body (for local governments). Since 1997, residents of small cities are permitted to vote on their school budgets.

[13] The New York State Assembly’s “Catalog of State and Federal Programs” (2007) provides a starting point for identifying any differences in assistance to a city versus a village under an array of state and federal programs.