As Richard Nathan noted earlier this month in this blog, the Trump administration is soon approaching a fork in the road on the Affordable Care Act (ACA). Up until this point, the Trump administration has been straddling the fence, giving signs at some points that it wants to act in a “business as usual” mode to preserve the law’s status quo and acting at other points as if it wants to actively undermine the ACA and disrupt its implementation. Preserving the status quo would allow the Trump administration to more credibly argue that the ACA has failed on its own, while disrupting the law’s implementation may result in voters blaming the new administration for any subsequent problems or failures.

Thanks to an upcoming federal budget deadline, however, the Trump administration may soon give an indication as to whether it wants to affirmatively embrace or eliminate a controversial provision of the ACA, known as Cost Sharing Reduction (CSR) subsidies, which lower out-of-pocket costs for lower-income Americans. Eliminating these CSR subsidies would increase uncertainty for the nation’s already beleaguered individual insurance markets and would likely lead to some combination of reduced coverage options and/or higher premiums for enrollees in the individual insurance market.

As their name indicates, CSR subsidies reduce out-of-pocket costs for qualifying enrollees in the individual insurance markets. These reductions can take the form of lower annual deductibles, lower copayments, and reduced annual out-of-pocket maximums. These subsidies, which are available on a “sliding scale” basis for enrollees making less than 250 percent of the federal poverty limit enrolled in “silver” plans, will benefit approximately seven million people in 2017. To cover the reduced out-of-pocket costs paid by enrollees, the federal government makes payments to insurance companies to subsidize costs.

These subsidies have not been without controversy, however. After the ACA’s enactment, congressional Republicans argued that the payments were illegally made without an explicit appropriation and sued to block the Obama administration’s payment of these subsidies to insurance companies (this lawsuit is now known as United States House of Representatives v. Price to reflect the new secretary of the Department of Health and Human Services, Thomas Price). In May 2016, a federal judge ruled in congressional Republicans’ favor and found that the payments to insurance companies had been made without the necessary appropriations, although the program had been authorized in federal law. The payments have continued, though, as the judge allowed for the payment of the subsidies until all appeals are exhausted. Since the Trump administration is now in the unusual position of defending the CSR subsidies in court, it could effectively dismantle this portion of the law by dropping the appeal of the lawsuit. It has not yet taken this step, however, and requested to extend the appeals process in February 2017, presumably as the administration bides its time while it seeks to enact legislative changes to the ACA.

By the end of this week, Congress and the president must act to provide funding for the federal government or face a government shutdown. This deadline may provide a clue as to how the Trump administration will manage the continued implementation of the ACA.

One option would be to preserve the status quo and continue to pay these subsidies to insurance companies. Although this would not eliminate all uncertainty or fix all of the problems facing the individual insurance market, it would, at a minimum, provide a level of year-to-year consistency in what could be a tumultuous year otherwise.

Another option, though, would be for the Trump administration to signal in the upcoming budget negotiations that it intends to cease the payment of these subsidies to insurance companies. If this occurs, the Trump administration would be taking real and meaningful steps to disrupt the individual insurance market that is critical to the success of the ACA.

While the exact chain of events that would stem from ending these payments is uncertain, it could include a number of consequences. Under current federal law, insurance companies in the individual market would be required to continue to offer plans that include these lower deductibles, lower copayments, and reduced out-of-pocket maximums. In this scenario, qualifying enrollees would continue to benefit from these CSRs, but the federal government would no longer reimburse insurance companies for the cost of providing them. Insurance companies may then withdraw from additional markets or charge higher premiums to recoup these lost payments from the federal government.

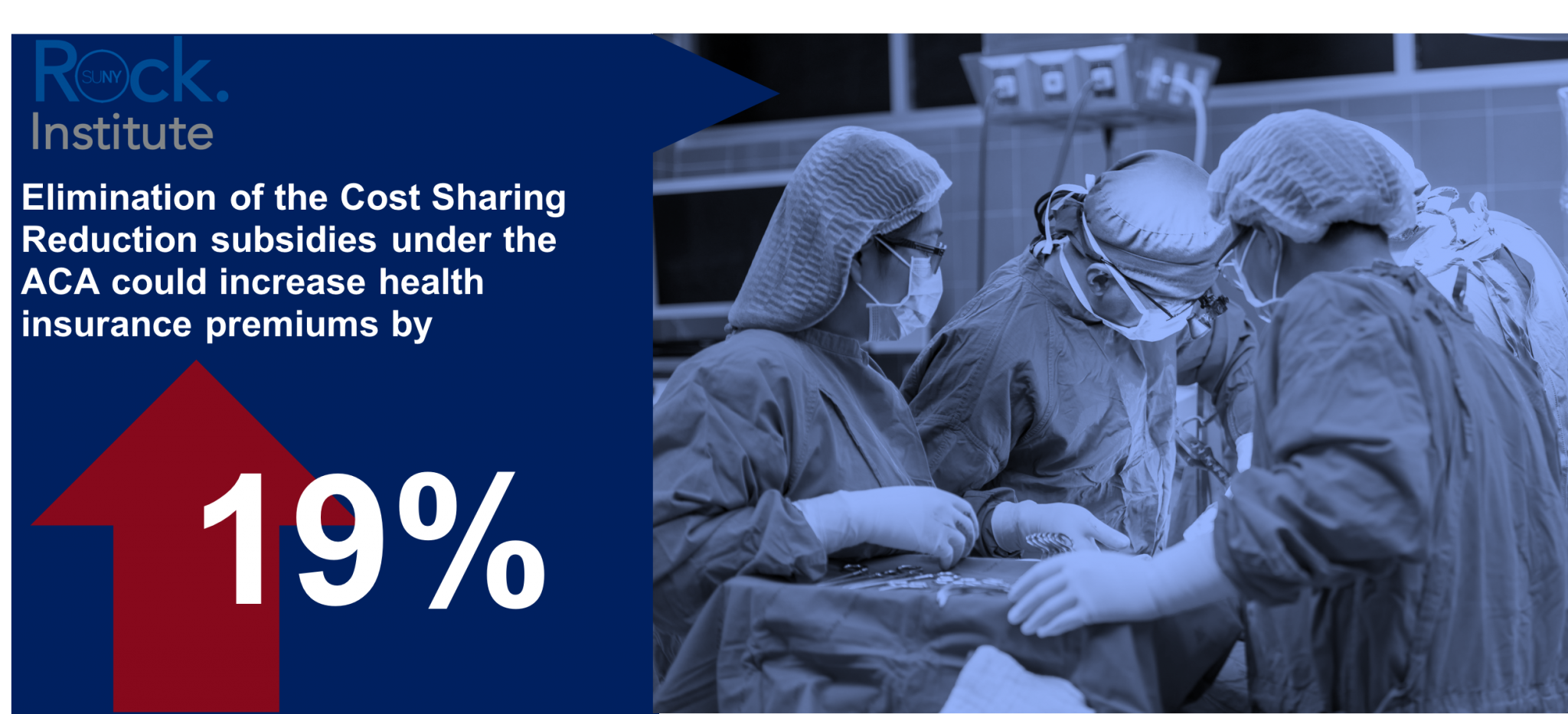

Enrollees who qualify for the lower out-of-pocket costs provided by CSRs also qualify for advance premium tax credits (APTCs), meaning increased premium costs for this group would be paid by the federal government. As a result, the effect of these higher premiums would only be truly felt by enrollees in the individual insurance market with higher incomes who do not qualify for CSRs or APTCs. Recent media reports suggest premiums could spike as much as 19 percent in this scenario. At a time when the individual insurance market is already beset with a great deal of turmoil and uncertainty, this increased cost could lead to additional enrollees terminating their coverage and further jeopardizing the stability of the entire individual insurance market.

The Trump administration will soon be forced to determine if it will take a hands-off approach to the ACA’s implementation or if it will actively undermine the law. The discussion around CSR subsidies in the upcoming budget negotiations will provide us with a clue to which approach they will take.